September 12, 2025

Today’s report was neutral for corn and soybeans and bearish for wheat relative to pre-report expectations. Today’s report included objective field level data for corn and soybean yield projections. Market attention will focus on developing trade relations and its impact on forward export sales, harvest progress, and yield results coming out of the fields in the coming weeks.

Corn

For corn, the domestic 2025/26 balance sheet called for larger supplies, larger exports, and a slight reduction in ending stocks. Corn production was increased as a 2.1 bushel reduction in yield was more than offset by a 1.3 million acre increase in harvested area. Pegged at 186.7 bushels per acre, this was slightly above analysts’ average pre-report estimate of 186.1 bushels per acre but within the range of estimates (182.7 to 189.0 bushel per acre range). Exports were raised by 100 million bushels to 2.975 billion. Ending stocks were reduced slightly to 2.110 billion bushels. This was slightly above analysts’ average pre-report estimate of 2.022 billion bushels but within range of estimates (1.748 to 2.344 billion range). Global corn production was lowered slightly, primarily on decreases in the EU and Russia. Global corn ending stocks were lowered to 281.4 million metric tons. This was slightly below analysts’ average pre-report estimate of 282.8 million metric tons but within the range of estimates (279.7 to 287.6 million range).

Corn yield reduced to 186.7 bushels per acre. If realized, would remain a record high:

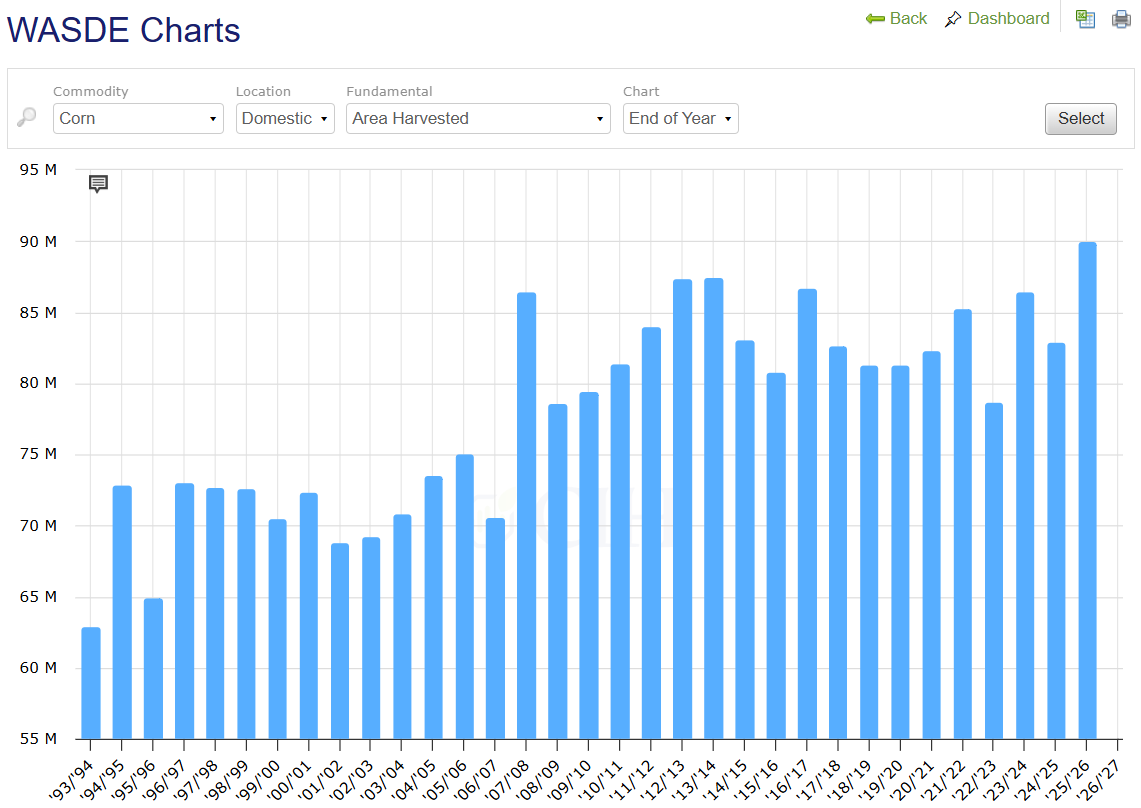

Corn harvested area increased from last month by 1.3 million acres:

Corn exports increased from last month based on strong pace of sales to date:

Soybeans

For soybeans, the domestic 2025/26 balance sheet called for higher production, lower exports, and higher ending stocks. Soybean production was increased slightly as an increase in harvested acres outweighed a decrease in yield. Pegged at 53.5 bushels per acre, the yield was slightly above analysts’ average pre-report estimate of 53.3 bushels per acre but within the range of estimates (52.9 to 54.0 bushel per acre range). Crush was raised by 15 million bushels driven by strong soybean meal exports. Soybean exports were reduced by 20 million bushels based on increased competition from Russia, Canada, and Argentina. Ending stocks were projected at 300 million bushels, up 10 million from last month, slightly above the average pre-report estimate of 293 million bushels, but well within the range of analysts pre-report estimates. Global soybean production was lowered as reductions in India, the EU, and Serbia offset higher production in the U.S. and Russia. Global ending stocks were lowered by 0.9 million metric tons to 124.0 million. This was below analysts’ average pre-report estimate of 125.4 million metric tons but within the range of estimates (123.2 to 127.0 million range).

Soybean exports pegged to be at lowest level since 2013/14:

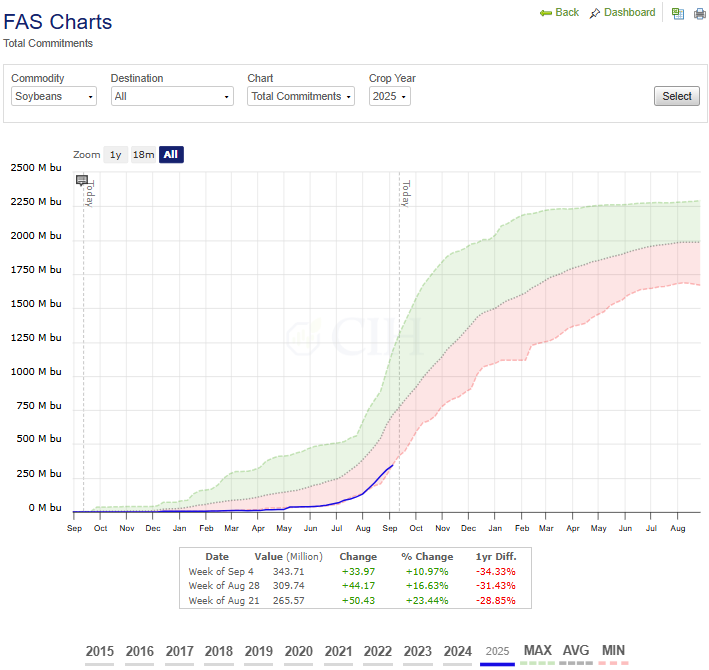

Total commitments of soybeans remain near 10-year lows due to China’s absence:

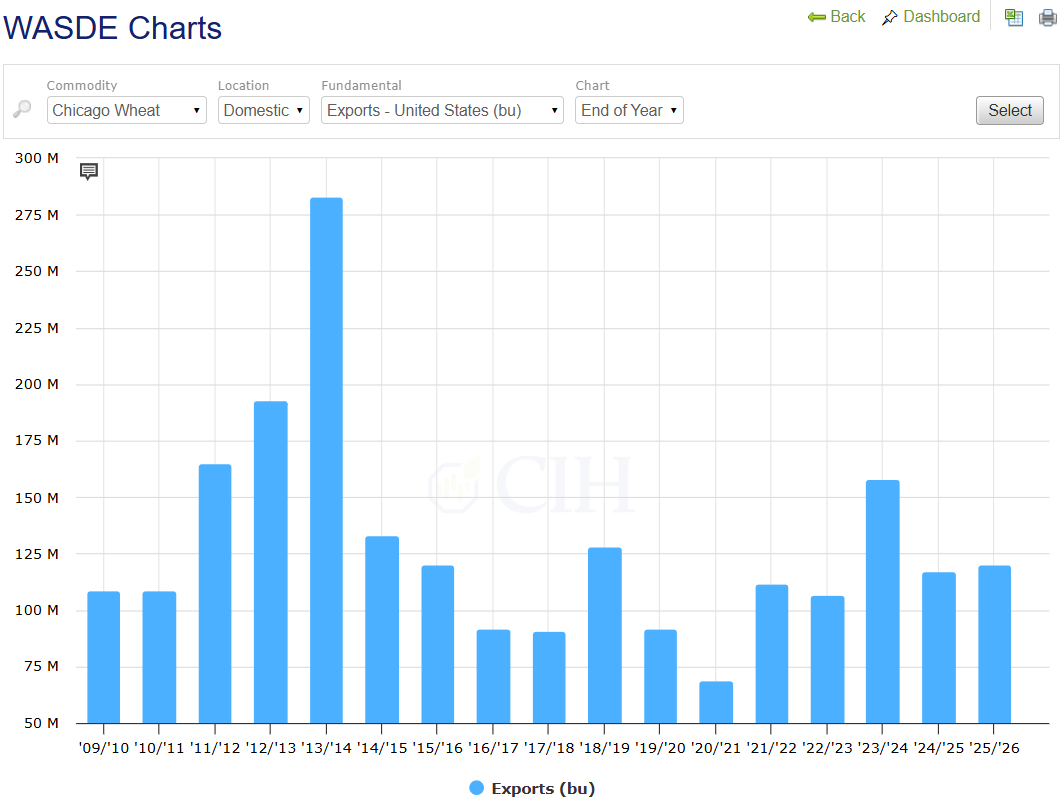

Wheat

For wheat, the domestic 2025/26 balance sheet called for higher exports due to increased shipments of Hard Red Winter wheat. Exports increased 25 million bushels and with no other changes lowers expected ending stocks by the same amount to 844 million bushels. This was below analysts’ average pre-report estimate of 862 million bushels but within the range of estimates (836 to 880 million range). USDA lowered the expected season-average price by $0.20 per bushel due to prices reported to date and expectations for futures and cash prices through the remainder of the year. On the global front, ending stocks are forecast to be higher by nearly 4 million metric tons due to large increases in expected global production. Australian production was increased 3.5 MMT on favorable conditions and reports indicated by recent ABARES forecasts. EU production is increased 1.9 MMT on harvest results, while Russian production was increased 1.5 MMT. Offsetting the 9.3 MMT increase in production were large increases feed and residual usage in several countries. Exports are expected to increase in Australian and the U.S. Global ending stocks are forecast at 264.06 MMT, above analysts’ average pre-report estimate of 260.8 million metric tons (258.4 to 263.0 million range).

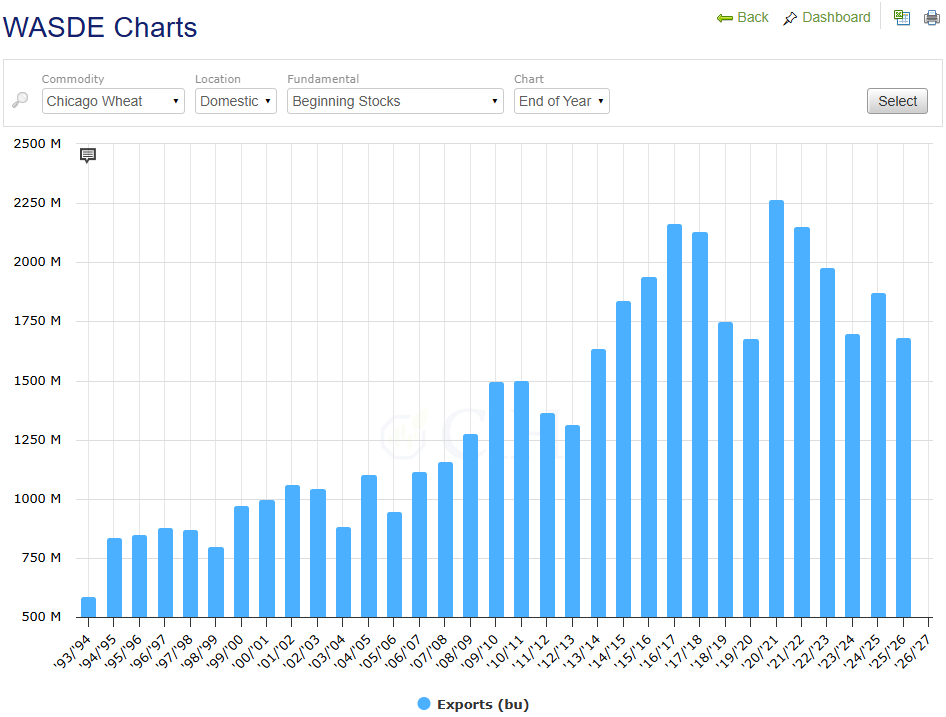

All wheat exports increased based on strong shipments of HRW:

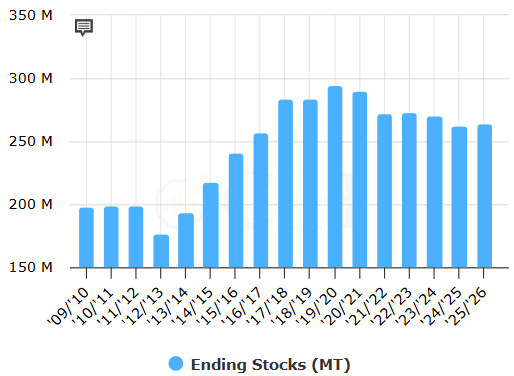

Global ending stocks increased from last month: