December 09, 2025

Today’s report was bullish for corn, neutral for soybeans, and neutral to negative for wheat relative to pre-report expectations. With the January report featuring more potential for changes to the balance sheet given the release of final production and quarterly stocks, USDA made only minor adjustments this month to supply and demand forecasts. Market attention will continue focus on developing South American crops and production potential along with monitoring the pace of soybean sales and shipments to China with expectations for significant volumes in the coming weeks.

Corn

For corn, the domestic 2025/26 balance sheet called for higher exports and lower ending stocks. Exports were raised 125 million bushels to 3.2 billion bushels reflecting shipments to date. USDA noted export inspection data showed robust foreign demand during November, implying that total shipments during the Sep-Nov quarter (Q1 of marketing year) will likely exceed 800 million bushels and surpass the prior high set in 2007. With no other changes noted to the domestic balance sheet, ending stocks were forecast to decline a corresponding 125 million bushels to 2.029 billion and below the range of pre-report estimates (avg. 2.166, range: 2.037-2.376). On the World balance sheet, global corn production was lowered as a 3 million metric ton drop in Ukraine’s output more than offset a 1 million metric ton increase projected for the EU. USDA noted that corn production in Ukraine is sharply lower due to reductions in both area and yield based on government reported data to date, where harvest has been slow due to wet conditions in key growing areas. Global corn ending stocks were lowered to 279.2 million metric tons from 281.3 million in November. This was below analysts’ average pre-report estimate of 281.3 million metric tons and on the bottom end of the range of estimates (279.0-283.0 million range).

Corn exports raised 125 million bushels to 3.2 billion, implying record Q1 shipments:

YTD corn export shipments have far exceeded the pace needed to reach USDA’s forecast, signaling an increase was forthcoming to projected exports:

Soybeans

For soybeans, the domestic 2025/26 balance sheet was left completely unchanged, with ending stocks remaining at a projected 290 million bushels, below the average pre-report estimate but within the range of estimates (avg. 309, range: 250-385). Likewise, no changes were noted on the domestic balance sheet for either soybean meal or soybean oil this month. Global soybean production was raised 800,000 metric tons from last month on higher crops for Russia and India but lower output in Canada and Ukraine. No production changes were noted for either Brazil or Argentina, and China’s import forecast was likewise left unchanged. Global soybean ending stocks were raised 400,000 metric tons to 122.4 million based on higher stocks for Brazil and Russia. This was below analysts’ average pre-report estimate of 122.8 million metric tons but within the range of estimates (121.6-125.0 million range).

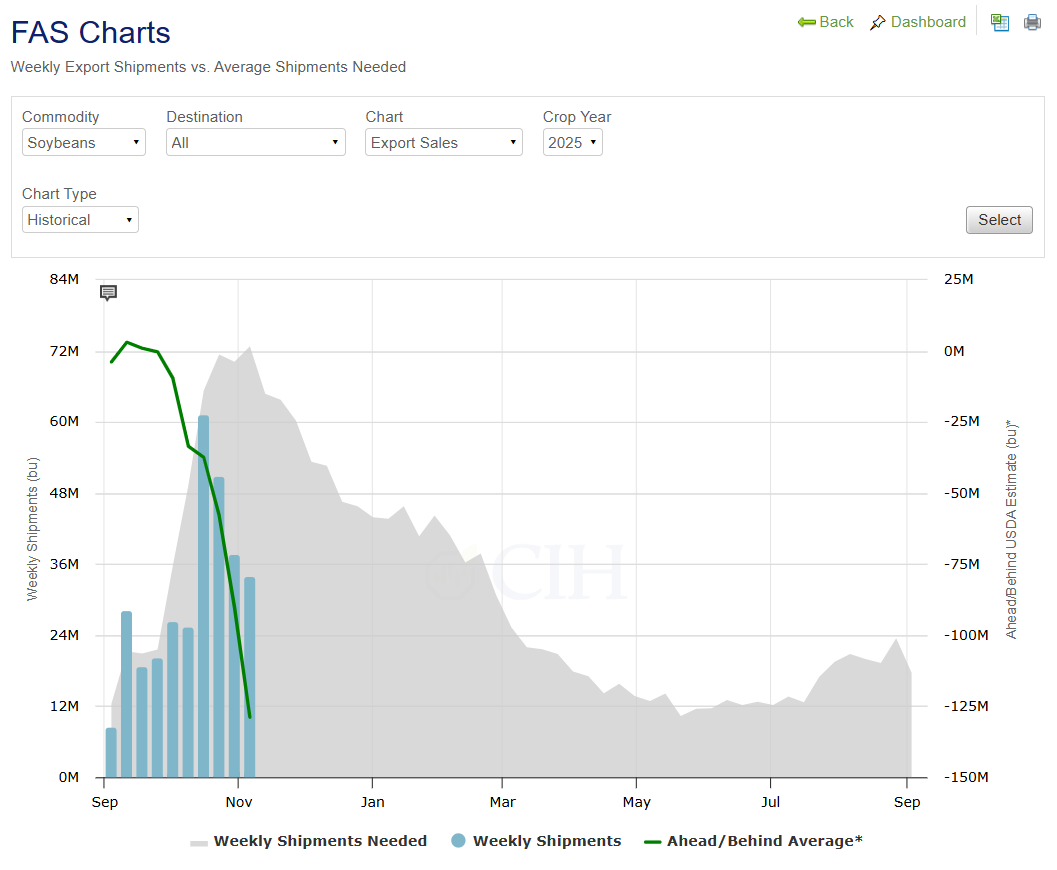

Despite a recent pickup in export commitments to China, soybean export sales remain well below the pace needed to reach the USDA forecast:

Total commitments of soybeans remain below 10-year lows despite recent sales activity to China:

Wheat

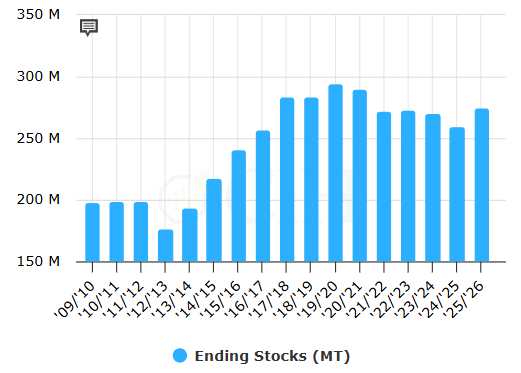

Similar to soybeans, USDA made no changes to the domestic balance sheet for wheat this month, with ending stocks still projected at 901 million bushels which was above the analysts’ average pre-report estimate of 893 million bushels and on the high end of the range of estimates (846-906 million range). Negativity primarily stemmed from the world balance sheet, with global wheat supplies projected to increase 7.5 million metric tons to 1,097.8 million on larger production from several main exporting countries. Canada’s wheat output was raised 3 million metric tons to a record 40 million on the final 2025/26 production forecast from Stats Canada. Argentina was increased 2 million metric tons to a record 24 million on widespread favorable conditions throughout the growing season, especially in Buenos Aires, the largest wheat producing region. The EU wheat crop was raised 1.7 million metric tons to 144 million on updated official government statistics for several countries within the bloc. Wheat production in both Australia and Russia were also increased 1 million metric tons from November to 37 million and 87.5 million, respectively. World wheat ending stocks were raised 3.4 million metric tons to 274.9 million, above analysts’ average pre-report estimate of 272.6 million metric tons and on the high end of the range of expectations (270.9-275.0 million range). This is the largest stocks level since 2020/21.

Global ending stocks projected to be the largest since the 2020/21crop year: