August 12, 2025

Relative to trade expectations, today’s report was bearish for corn, bullish for soybeans and neutral for wheat. This was the first WASDE report of the 2025-26 season to incorporate field surveys to model the yield outlook for U.S. corn and soybean production, which can lead to added volatility in the market given increased probability for deviations from the econometric model used in the May-July reports. Market attention will continue to focus on crop progress and weather’s impact on yield potential across the U.S. Midwest as we approach harvest.

Corn

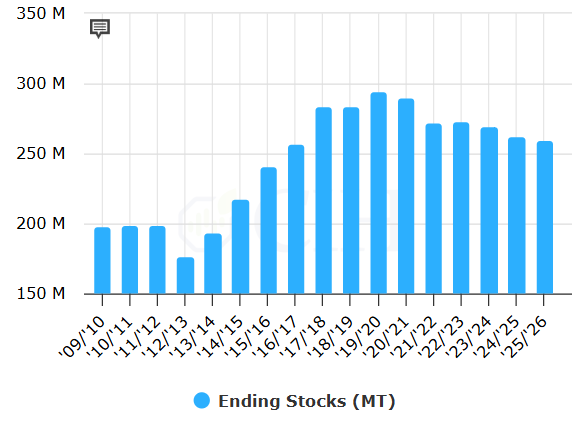

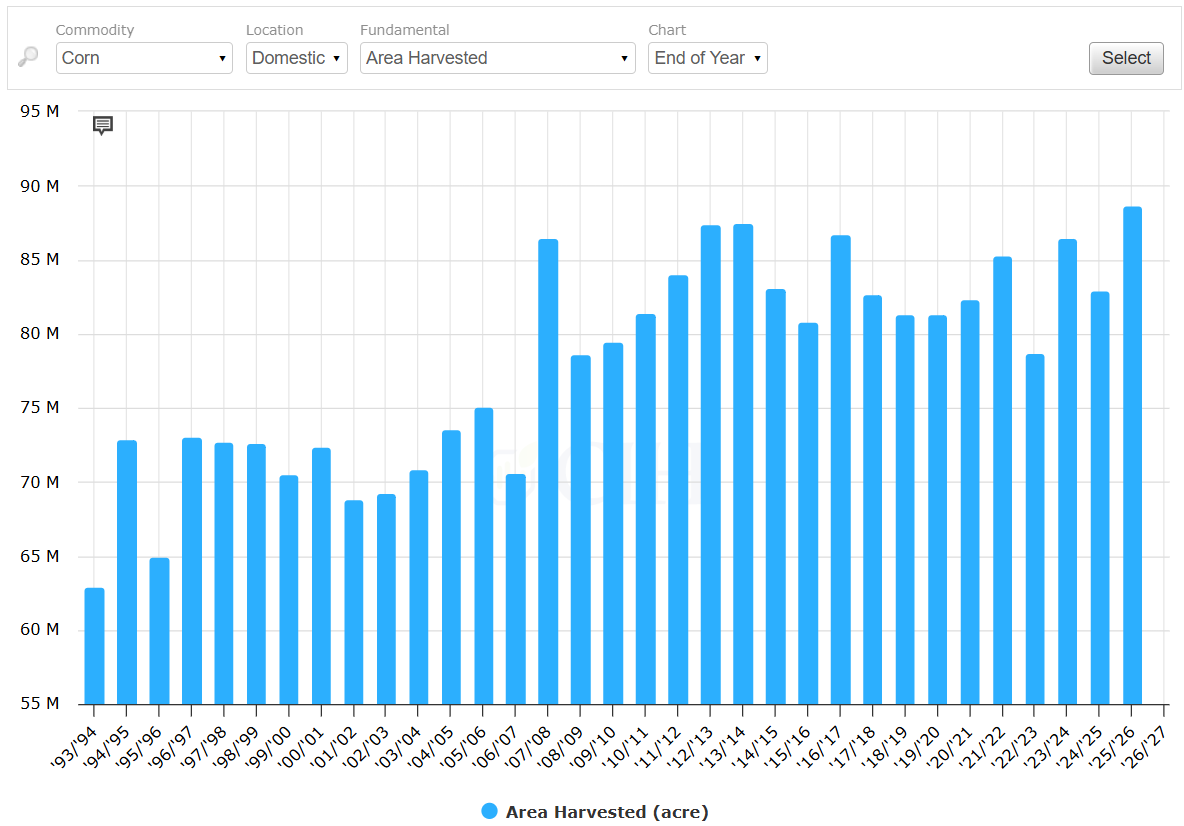

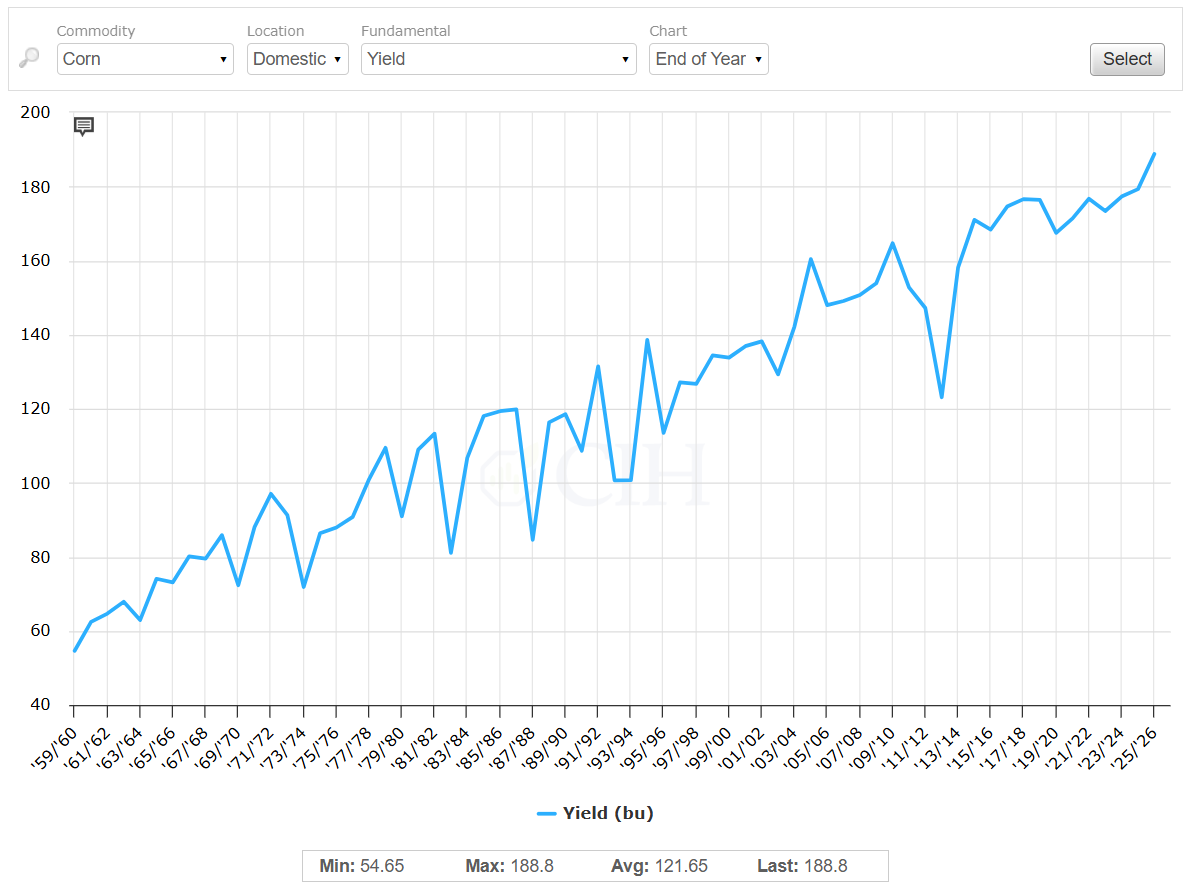

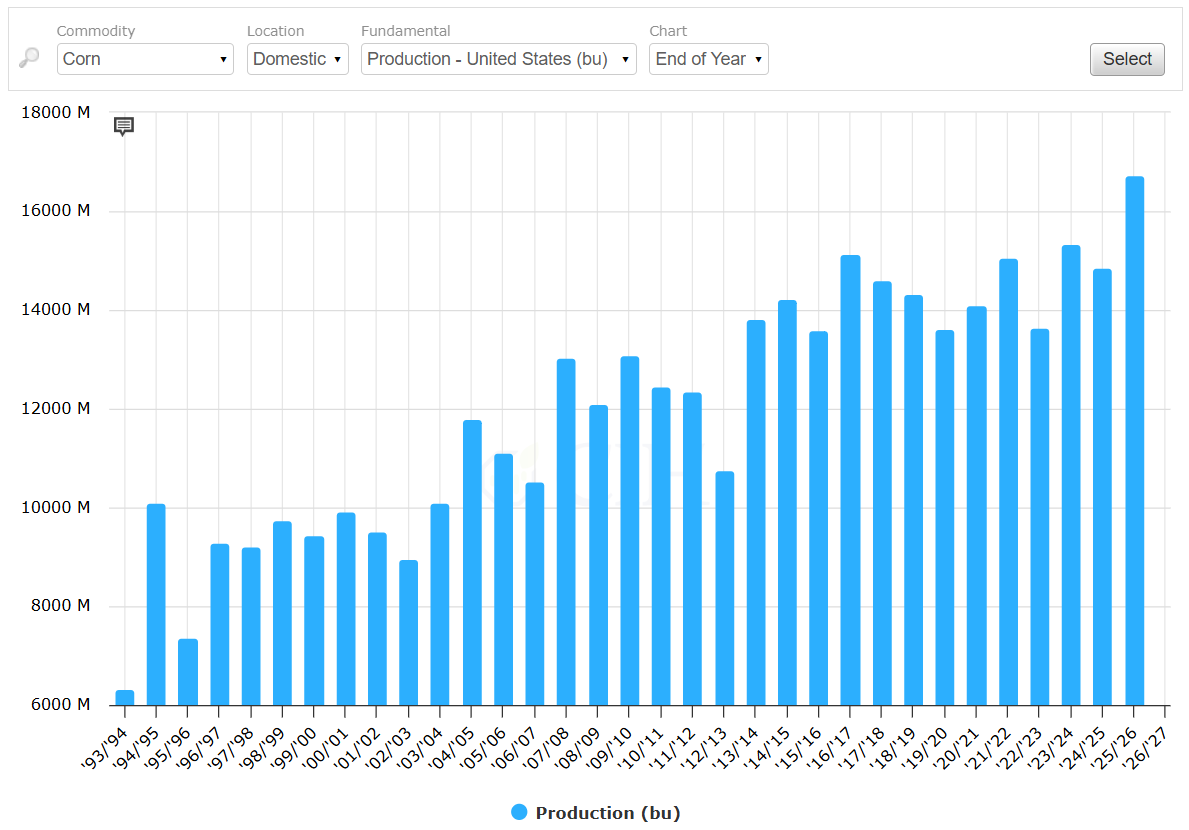

Corn production was estimated at 16.742 billion bushels, up 1.037 billion bushels from July based on both larger acreage and an increase in projected yields. The estimate was significantly higher than the average trade estimate of 15.991 billion bushels and outside the range of pre-report trade expectations between 15.705 and 16.323 billion bushels. Planted and harvested acres were raised to 97.3 (+2.1) and 88.7 (+1.9) million, respectively, with the national yield forecast at 188.8 bushels per acre, up 7.8 from last month. If realized, U.S. production would be 1.4 billion bushels more than the prior record set in 2023-24. Slightly offsetting the increase in production, total corn use for the 2025-26 season was raised 545 million bushels from last month to 15.955 billion. Feed and residual use is increased 250 million bushels to 6.1 billion based on a larger crop and lower expected prices. Corn used for glucose and dextrose is projected lower based on observed use during 2024-25. Corn used for ethanol for 2025-26 is raised 100 million bushels to 5.6 billion, and exports are projected 200 million bushels higher to a record 2.9 billion bushels reflecting U.S. export competitiveness and expectations for relatively low world market prices. Ending stocks were raised 457 million bushels from July to 2.117 billion bushels, above the average pre-report estimate of 1.916 billion bushels but within the range of estimates (1.660 to 2.333 billion range). The average farm price was lowered to $3.90/bushel from $4.20 last month, in line with a long-term regression given the projected stocks/use ratio 13.3%. On the world balance sheet, 2025-26 ending stocks are projected at 282.5 million metric tons, up from 272.1 million in July, higher than the average trade estimate of 279.1 million, but within the range of analysts’ pre-report estimates (272.6 to 283.9 million range).

Harvested area at 88.7 million acres would be a new record high and up sharply from 82.9 million last season:

Yield at 188.8 bushels per acre would be a new record high and above the long-term trendline:

Production at 16.742 billion bushels would be a new record high and well above the previous record in 2023-24:

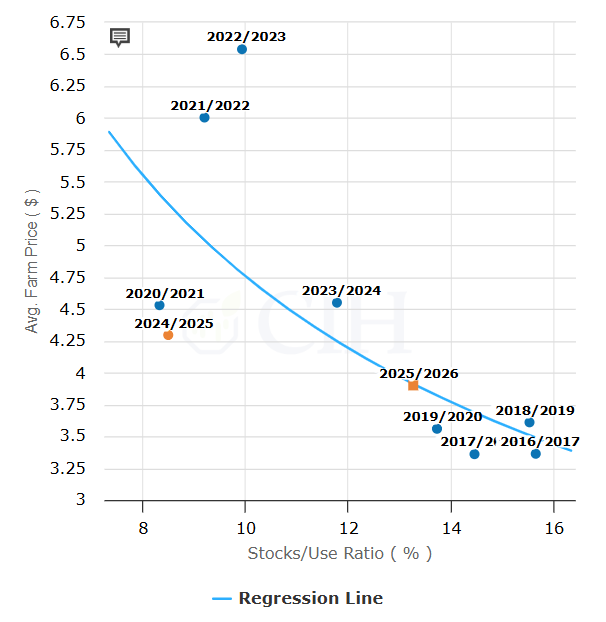

Regression of U.S. domestic stocks/use ratio to average farm price:

Soybean

Soybean production was estimated at 4.292 billion bushels, down 43 million from July, as lower planted and harvested acreage offset an increased yield estimate. The U.S. production figure was below the average trade estimate of 4.371 billion, and on the lower end of the range of pre-report estimates (4.290 to 4.439 billion range). Planted and harvested area was lowered to 80.9 (-2.5) and 80.1 (-2.4) million acres, respectively, with yield raised to 53.6 bushels per acre, up 1.1 from last month, above the average trade estimate of 53.0 bushels per acre, and on the high end of the pre-report range of estimates (52.0 to 53.7 range). Beginning stocks were lowered 20 million bushels on an increase to crush and exports in the 2024-25 crop year. Given the lower supply and slow pace of export sales to date, 2025-26 exports were lowered 40 million bushels from last month while the new-crop crush estimate was left unchanged. U.S. ending stocks are projected at 290 million bushels, down 20 million from July, below the average trade estimate of 359 million and below the range of pre-report estimates (310 to 416 million range). The average farm price was left unchanged at $10.10/bushel while the soybean meal price is forecast down $10 from July at $280/ton and the average soybean oil price forecast was left unchanged at 53 cents/lb. On the world balance sheet, global ending stocks were lowered to 124.9 million metric tons, below the average pre-report estimate of 127.9 million, and well below the range of analysts’ pre-report estimates (126.5 to 129.0 million range).

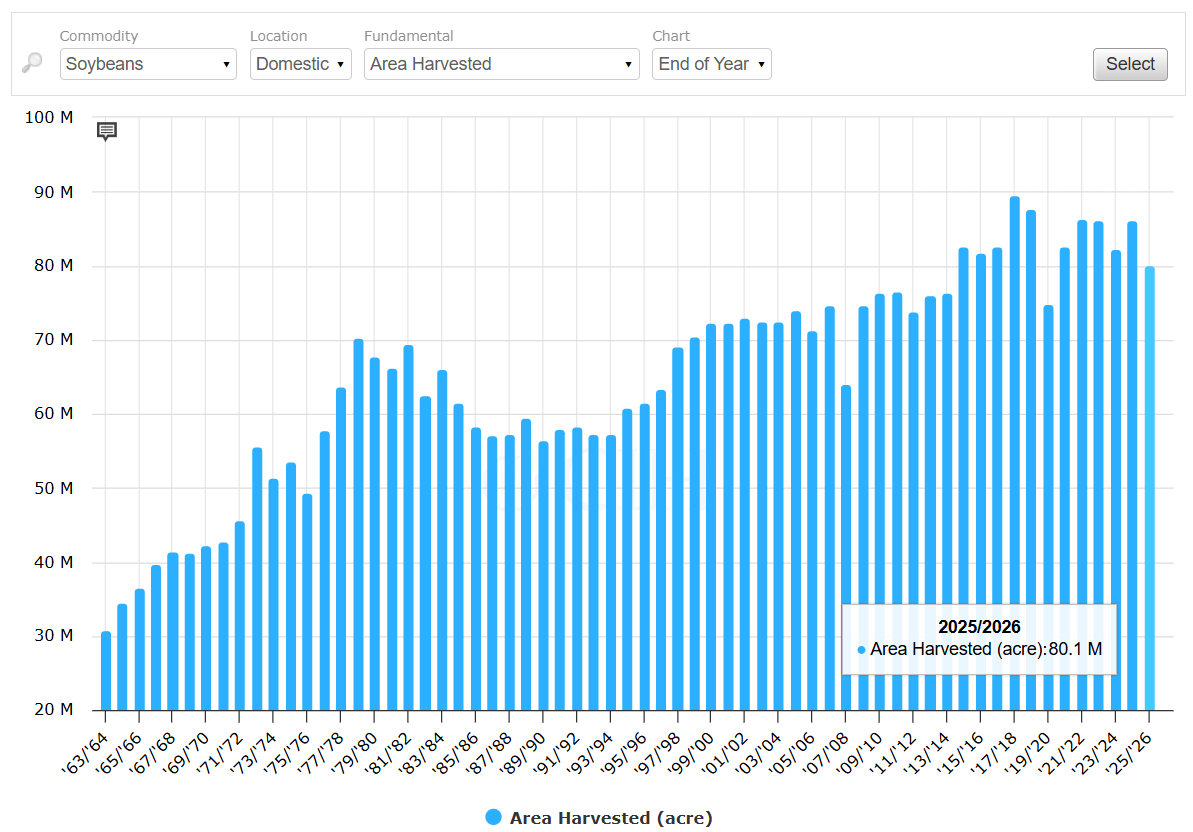

U.S. soybean harvested area at 80.1 million acres would be the lowest since 2019-20:

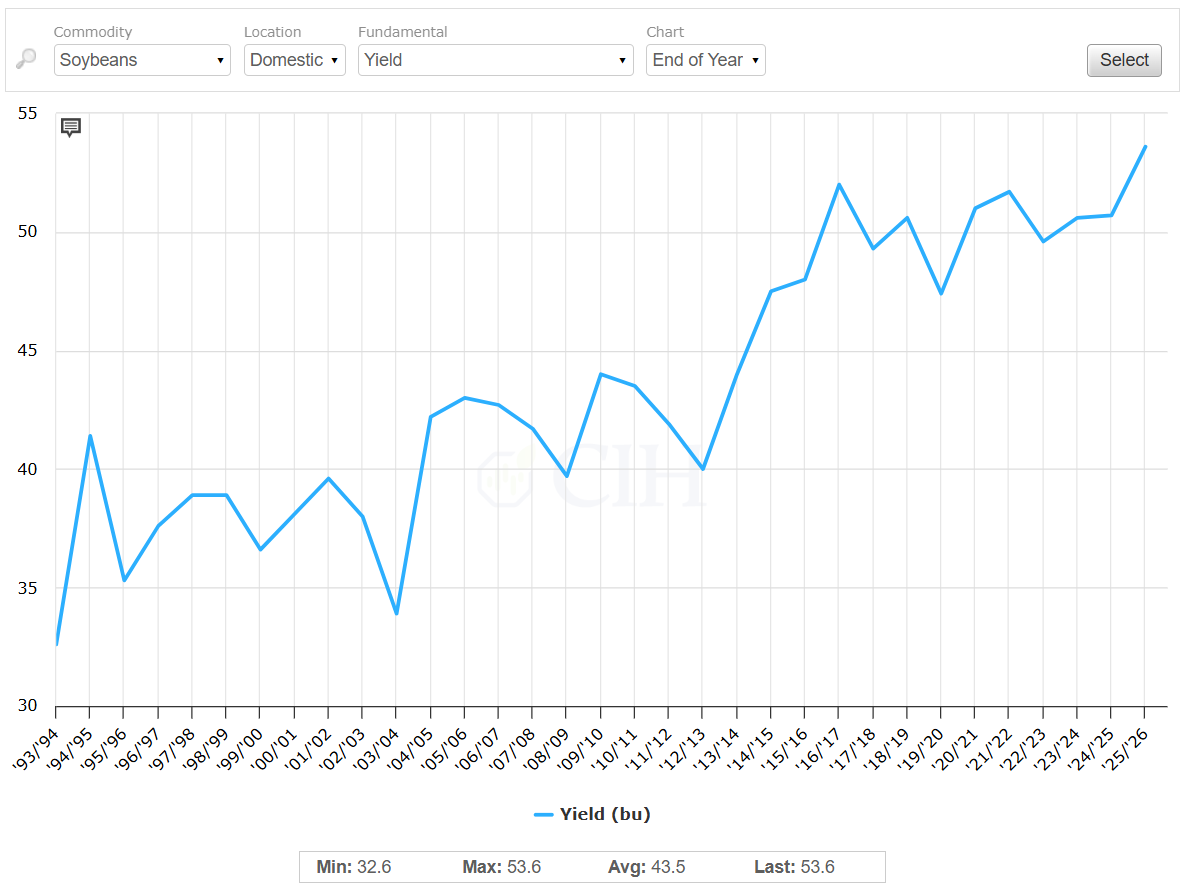

Yield at 53.6 bushels per acre would be a new record high:

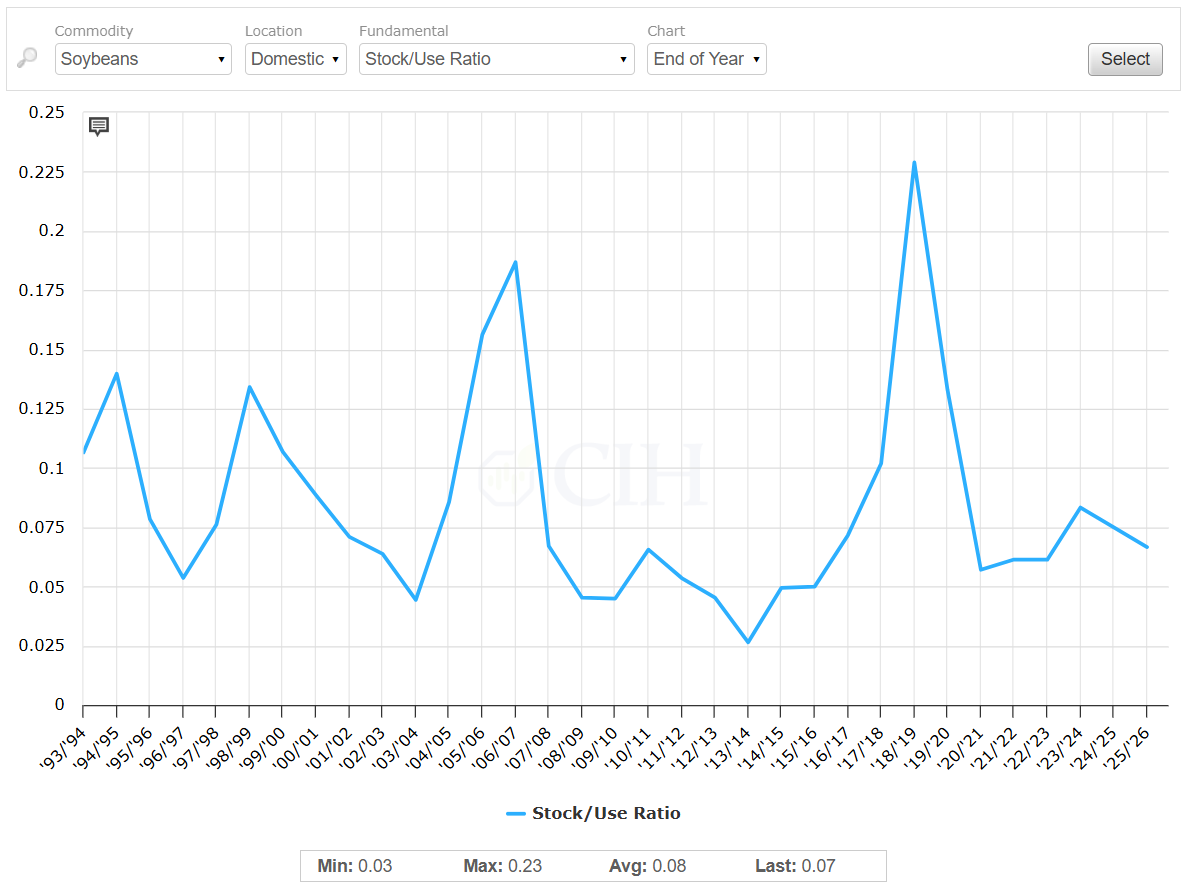

The U.S. soybean stocks/use ratio at 6.7% is down from last year and below average but remains above the lows from the 2020-23 crop years:

Wheat

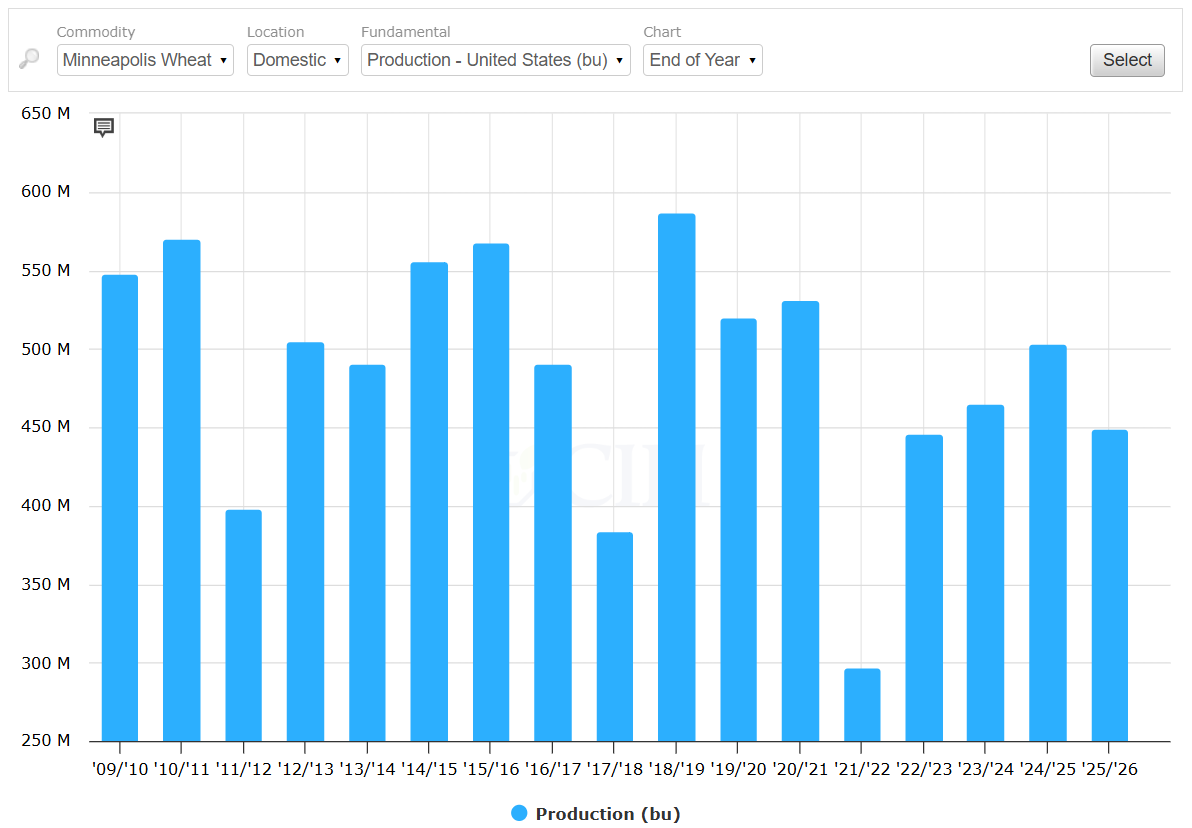

Total U.S. wheat production was lowered 2 million bushels from last month to 1.927 billion bushels, very close to the average pre-report trade estimate of 1.925 billion (1.879 to 1.950 billion range). By class, HRW wheat production was pegged at 769 million bushels, up 14 million from July (average: 758; range: 748-774); SRW production was pegged at 339 million bushels, up 2 million from July (average: 338; range: 336-345); WWW production was estimated at 247 million bushels, down 7 million from July (average: 252; range: 243-260); other spring wheat was projected at 485 million bushels, down 19 million from July (average: 497; range: 478-515); and durum wheat production was pegged at 87 million bushels, up 7 million from July (average: 80; range: 74-90). Domestic food use was lowered 5 million bushels based on the latest NASS Flour Millings Products report. Exports were raised 25 million bushels on the continued strong early pace of sales and shipments, particularly for HRW wheat. Projected ending stocks were reduced 21 million bushels from July to 869 million, below the average trade estimate of 885 million and on the lower end of the range of analysts’ pre-report estimates (860 to 920 million range). The global balance sheet called for reduced supplies and reduced ending stocks. Supplies were lowered 2.5 million metric tons to 1.07 billion on lower production for China, Brazil and Argentina that was only partly offset by a larger forecast for the EU. EU production was raised 1 million metric tons from last month to 138.3 million which would be the highest since 2021-22 as several months of favorable weather conditions have improved quality and yield prospects. Projected global ending stocks were lowered by 1.4 million metric tons to 260.1 million. This was below the analysts’ average pre-report estimate of 261.8 million metric tons and on the bottom end of the range of estimates (260.1 to 263.5 million range). Global ending stocks would be the lowest since the 2015-16 marketing year.

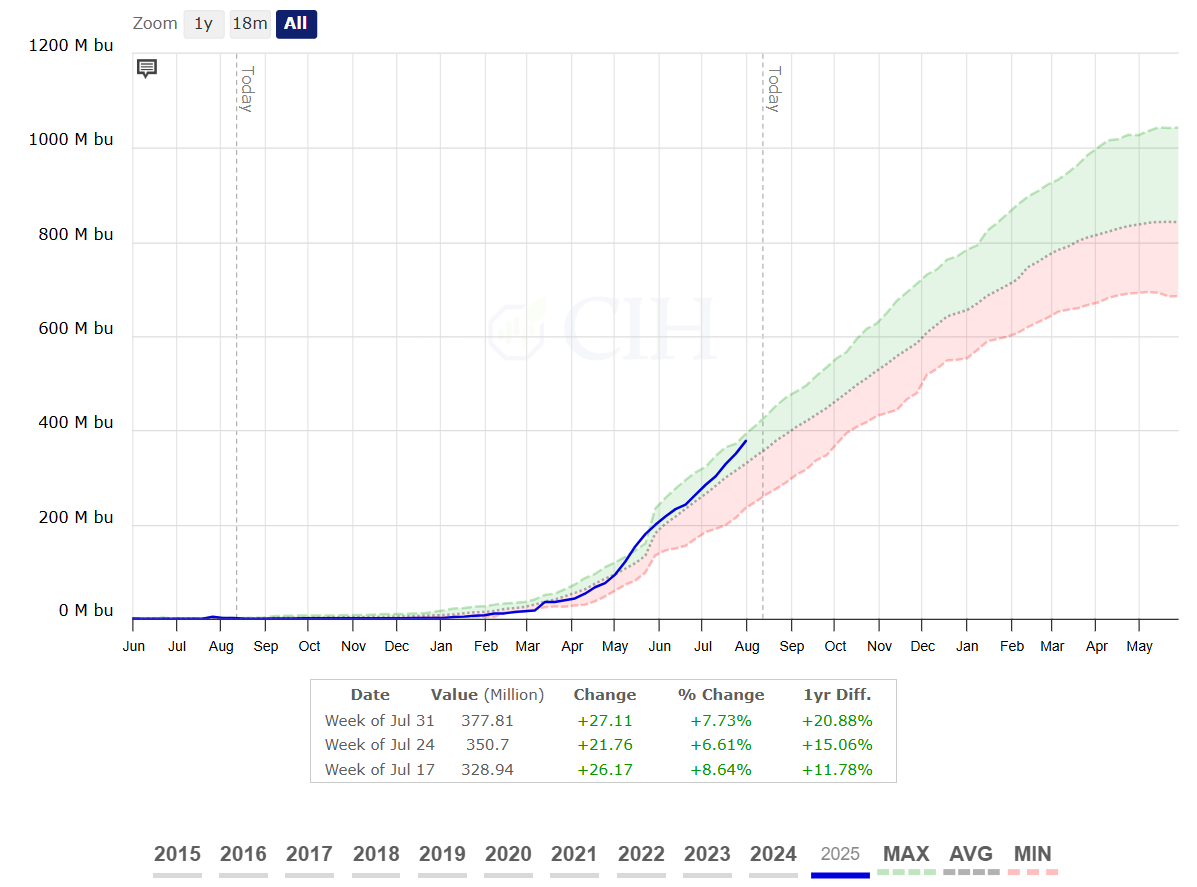

U.S. wheat exports raised 25 million bushels based on the pace of strong early season sales commitments:

Spring wheat production forecast down 54 million bushels from last year and the lowest in 3 years:

World ending stocks at 260.1 million metric tons would be the lowest since the 2015-16 crop year: