May 12, 2026

This report was considered bullish for wheat and soybeans while neutral for corn. The market’s focus will continue to eye planting progress, early season crop development and this week’s U.S./China meeting.

Corn

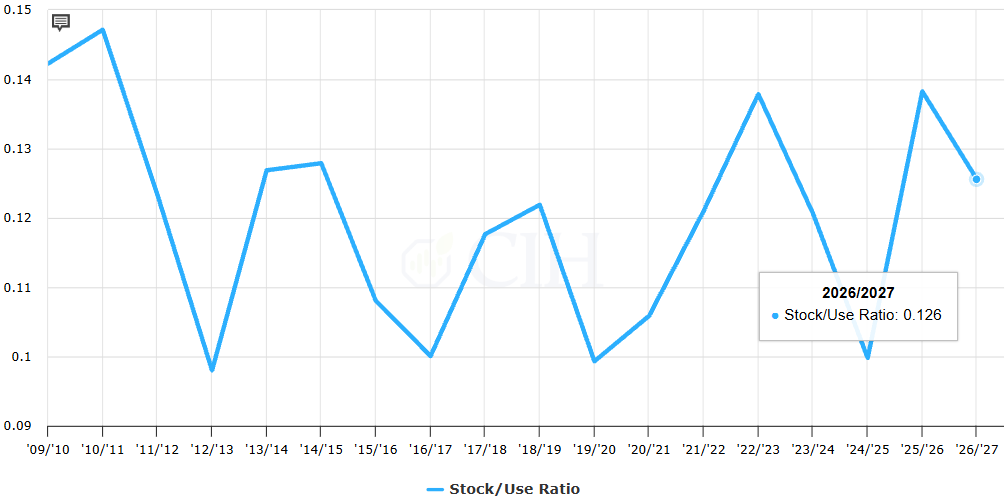

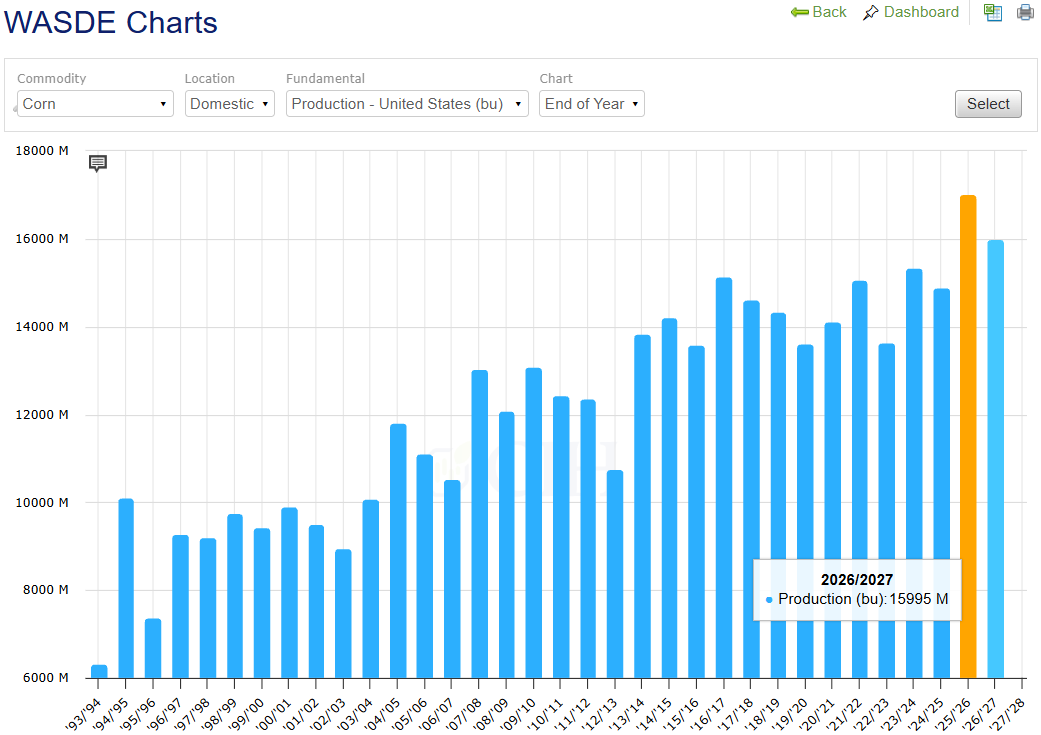

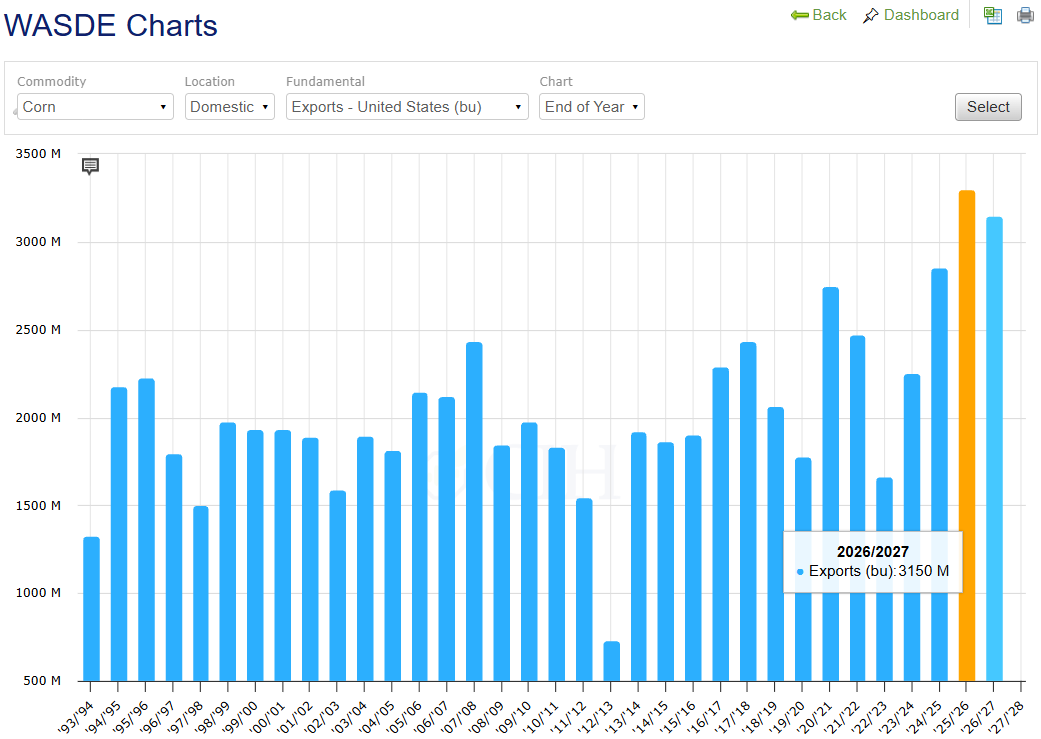

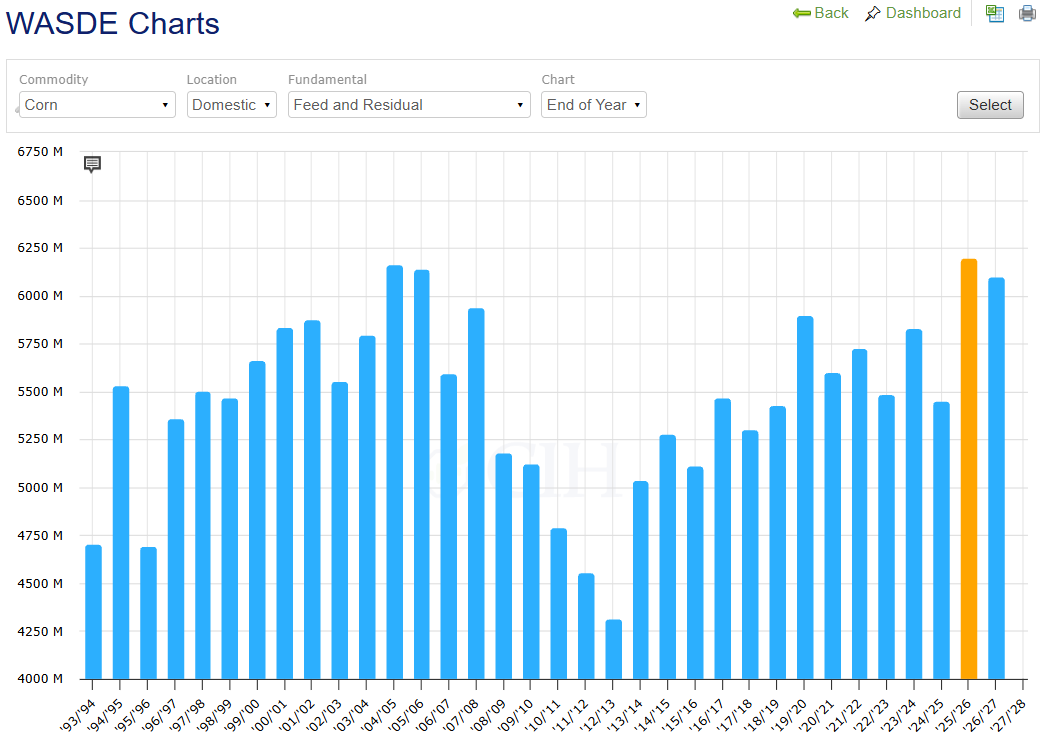

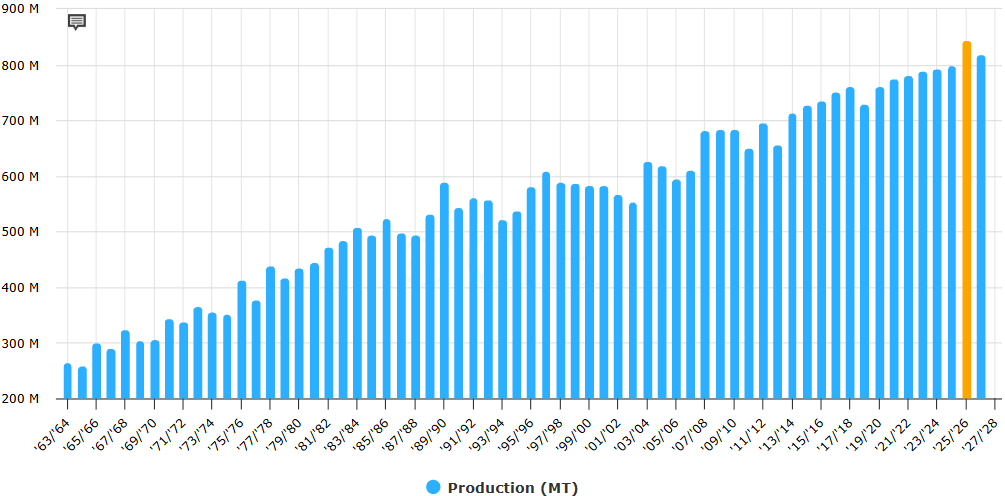

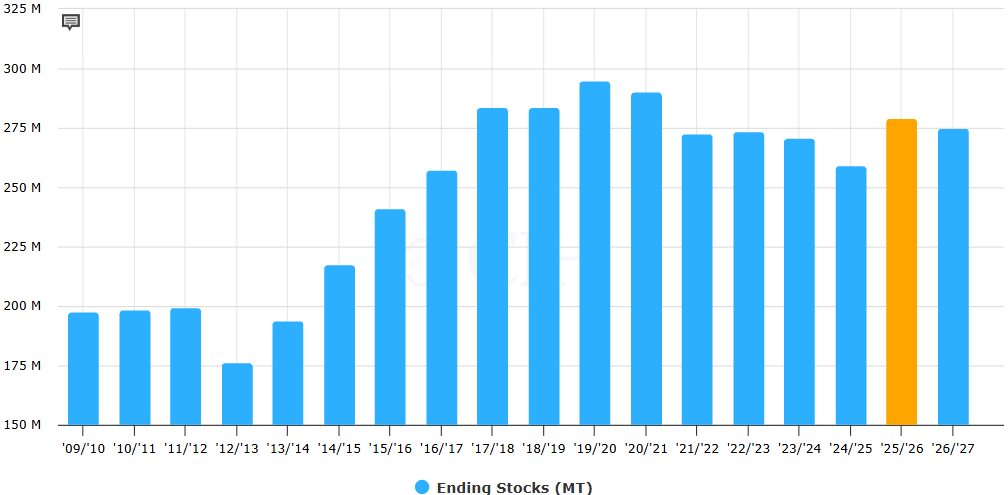

For corn, USDA’s first 2026/27 balance sheet held few surprises. Production is forecast at 15.995 billion bushels, slightly above pre-report estimates at 15.948 billion bushels, but within the range of estimates (15.819-16.011). National average yields are initially pegged at a weather-adjusted trend of 183.0 and are subject to change as the growing season advances. On the demand side of the balance sheet, exports are lowered by 150 million bushels from the 2025/26 crop year likely due to smaller expected production. While exports are projected to be lower than last season, if realized, this forecast would be the second largest on record. The U.S. is expected to remain the largest global exporter, despite growing competition from Brazil and Ukraine. USDA also pegs feed and residual use down from prior year due to smaller supplies. Initial new-crop ending stocks are forecast at 1.957 billion bushels, down 170 million bushels from the 2025/26 season. This puts the stocks-to-usage ratio at 12.1% compared to 13.0% in 2025/26.

On the world side, global ending stocks for the 2026/27 year are forecast lower by 19.41 MMT to 277.54 MMT due to decreases in production and increases in consumption. Production is forecast lower for the U.S., Argentine, South Africa, Mexico, Ukraine and Turkey. Partially offsetting are production increases for China, Brazil, Serbia, Kenya and Russia. Major exporter ending stocks are expected to fall slightly for the 2026/27 season, keeping the stocks-to-use ratio for that group at a relatively tight 8.0%, down from 8.4% last year.

Corn production forecast lower y/y by 1.026 billion bushels but still second-largest on record:

Corn exports expected to stay strong, but slightly lower than last year’s record:

Corn feed and residual use remains elevated compared to the last ten years, despite slightly higher prices:

Corn global ending stocks forecast lower:

Soybeans

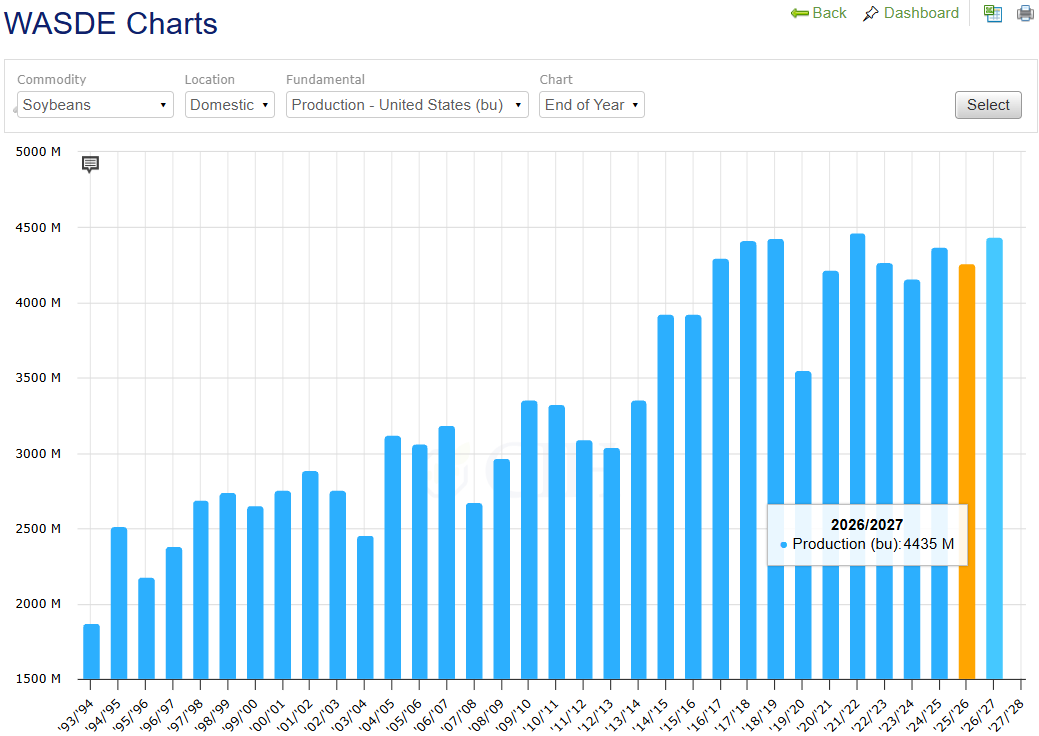

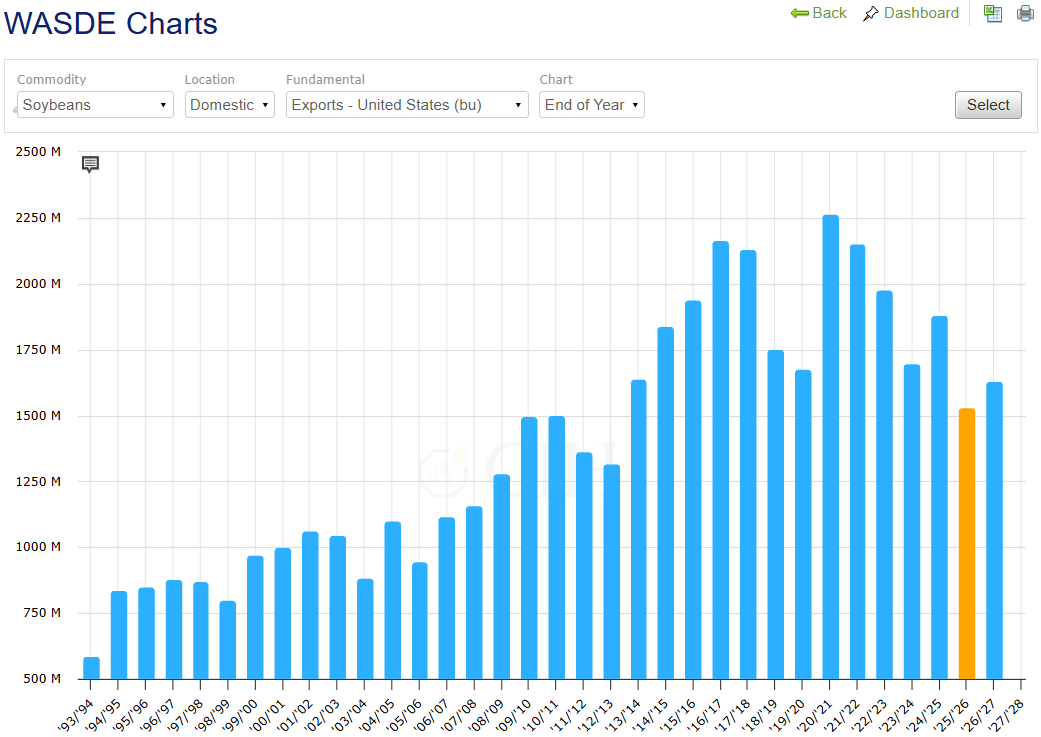

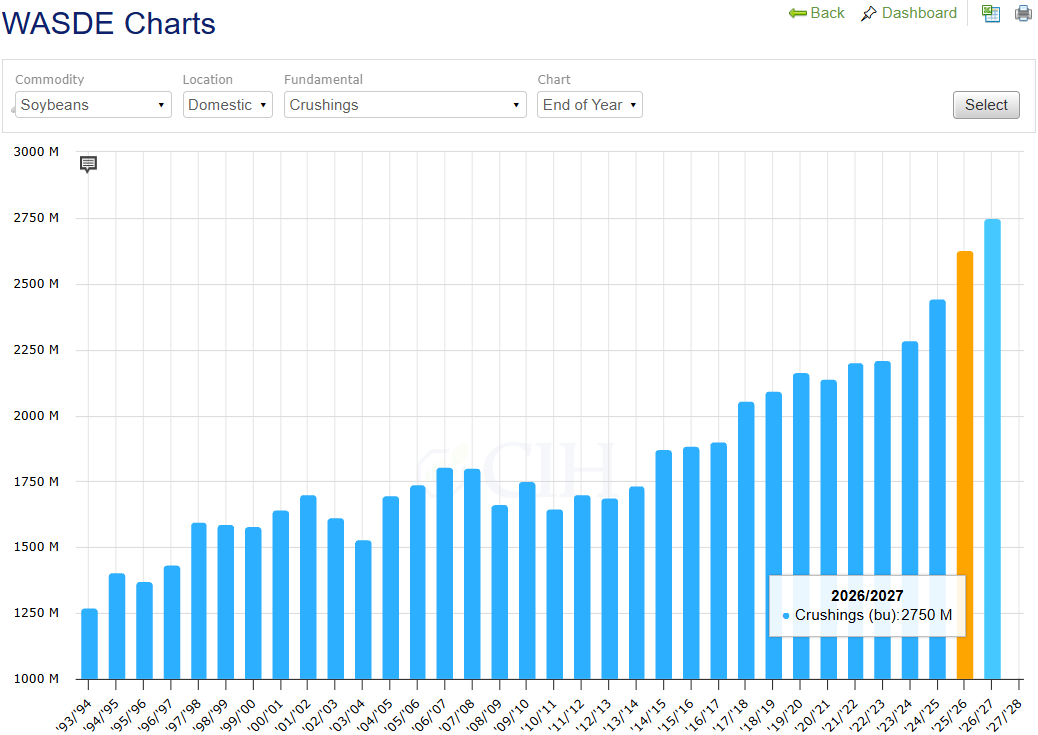

For soybeans, USDA’s first 2026/27 balance sheet showed increased supplies and demand. Production is forecast at 4.435 billion bushels, slightly below pre-report estimates at 4.45 billion bushels, but within the range of estimates (4.405-4.521). National average yields are initially pegged at a weather-adjusted trend of 53.0 and are subject to change as the growing season advances. On the demand side of the balance sheet, exports are raised 90 million bushels from the 2025/26 crop year due to “…an increase over 2025/26 when tariff measures curtailed shipments to China, the United States’ largest export market.” While exports are projected to be higher than last season, the U.S. share of global exports is expected to shrink due to larger South American supplies and increased domestic demand. Crush is forecast up 120 million bushels from the 2025/26 season due to favorable crush margins and strong forecasted demand for soybean oil as a feedstock. Soybean oil use for biodiesel is expected to increase by 3.6 billion pounds (+25%) from last year while exports are forecast to be down 800 million pounds as domestic demand crowds out volume available for export. The increased usage for biofuels is explained by EPA’s Renewable Volume Obligations for 2026 and 2027. Soybean meal domestic usage is expected to rise modestly, while exports are forecast to jump 1.9 million short tons.

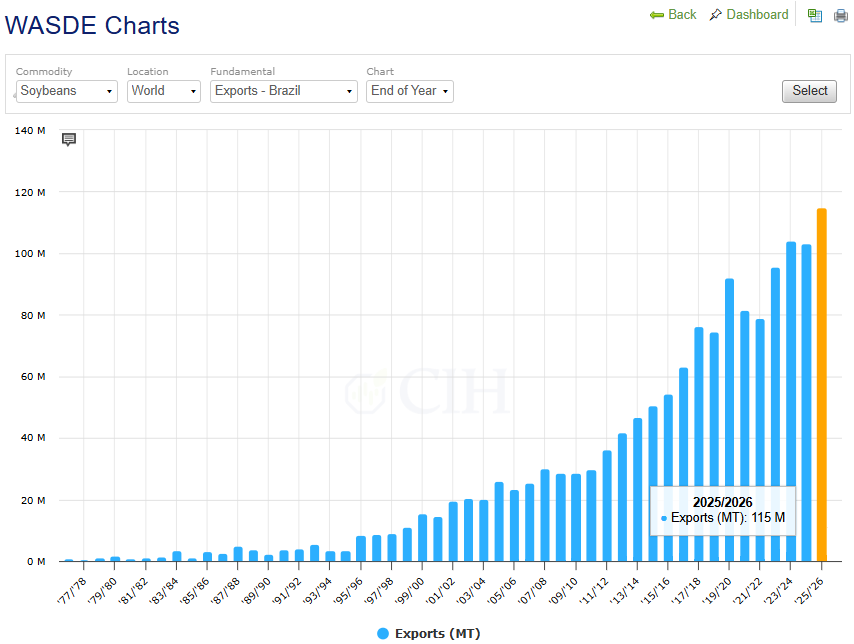

On the world side, global ending stocks for the 2026/27 year are forecast slightly lower to 124.78 MMT with larger production entirely offset by increased usage. Production is forecast to rise 6 MMT for Brazil to 186 MMT, 2 MMT for Argentina to 50 MMT and as mentioned by 4.7 MMT for the U.S. at 120.7 MMT. Chinese imports are forecast up 2 MMT to 114 MMT. Crush is estimated 13.6 MMT higher than last year: Brazil (+3.5 MMT), U.S. (+3.26 MMT), Argentina (+1.5 MMT). With ending stocks roughly unchanged and higher demand expected, the world stocks-to-use ratio is expected to decline to 28.3% versus 29.3% last year.

Soybean production forecast higher but within the range of the last ten years:

Soybean exports forecast higher than last year but second-lowest since 2013/14:

Soybean crush forecasted to be record large for the 6th straight year:

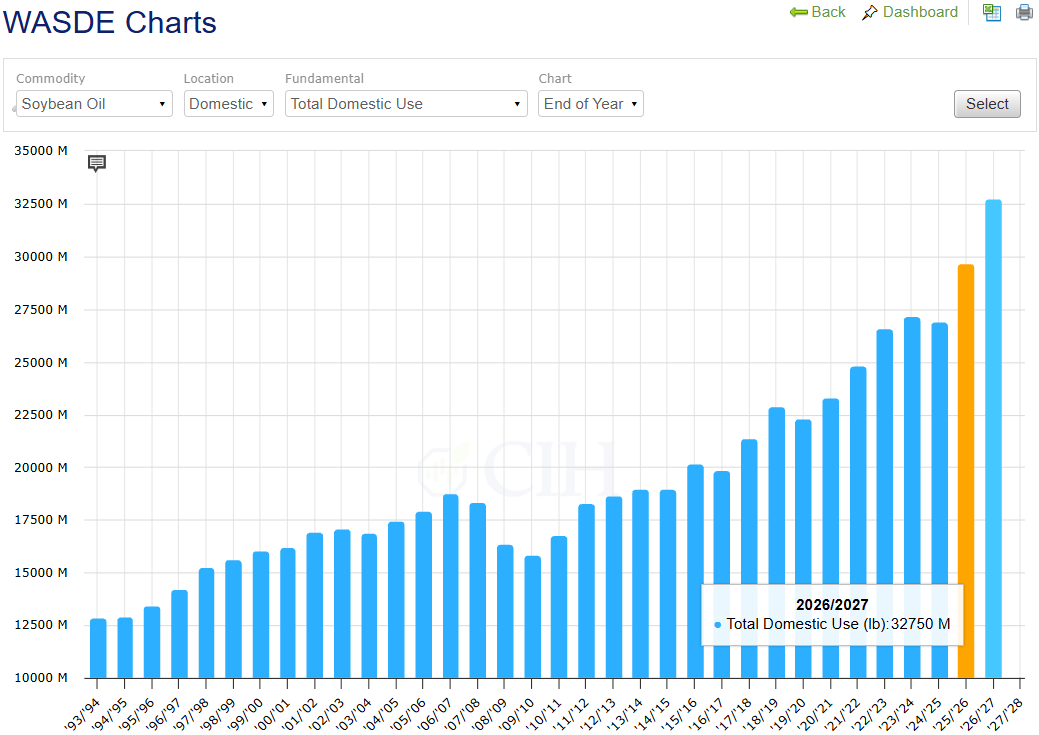

Soybean oil domestic use continues to rise due to biofuel production increases:

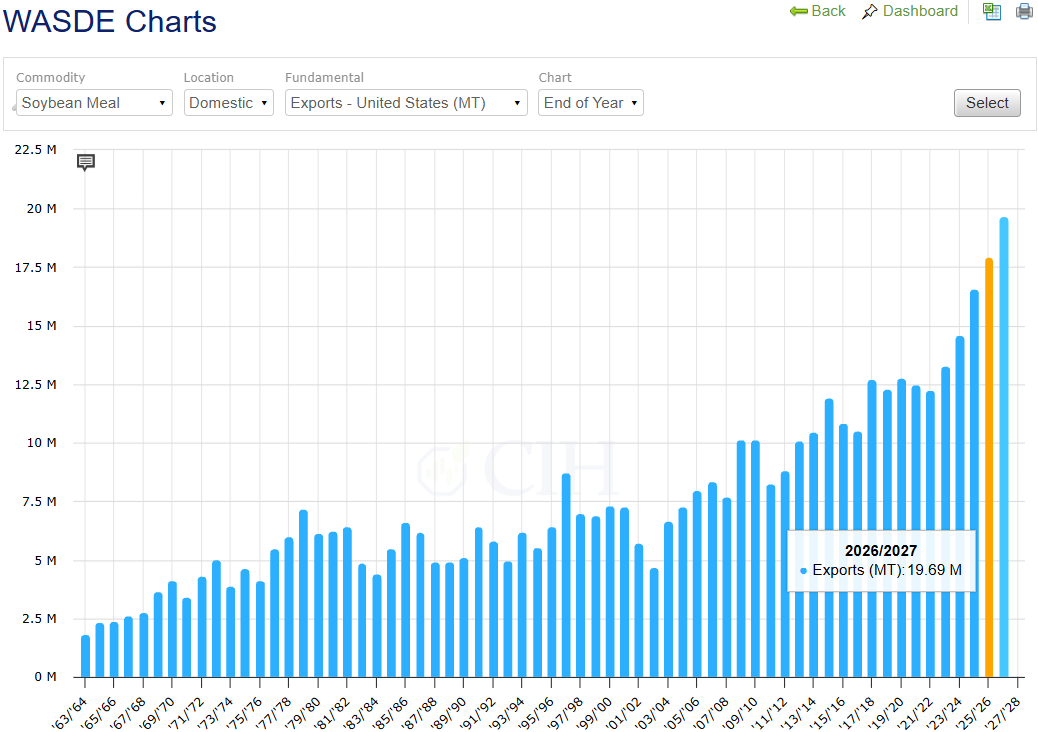

Soybean meal exports forecast to rise nearly 10% y/y:

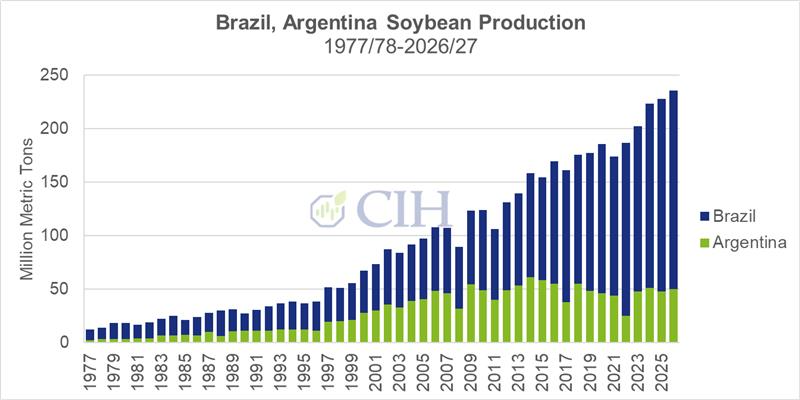

Combined Brazil and Argentine production expected to be record high:

Global stocks-to-use continues to tighten for major exporters:

Wheat

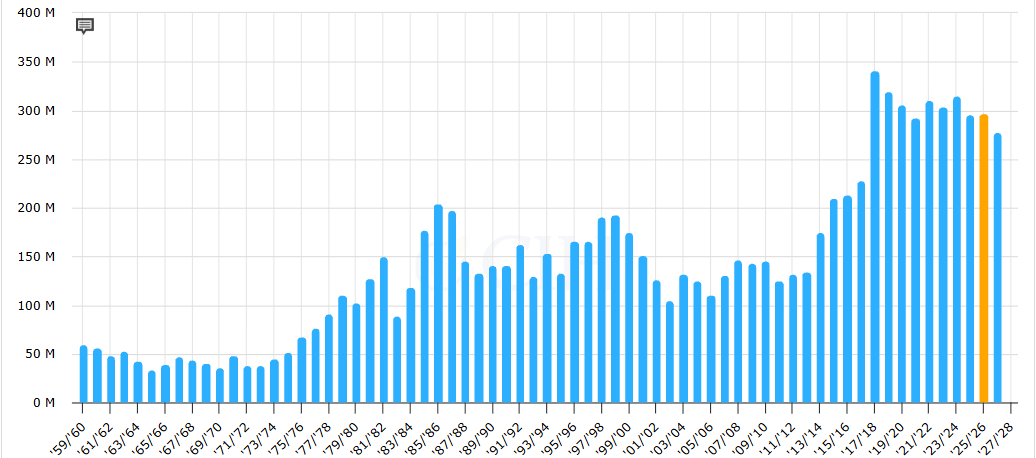

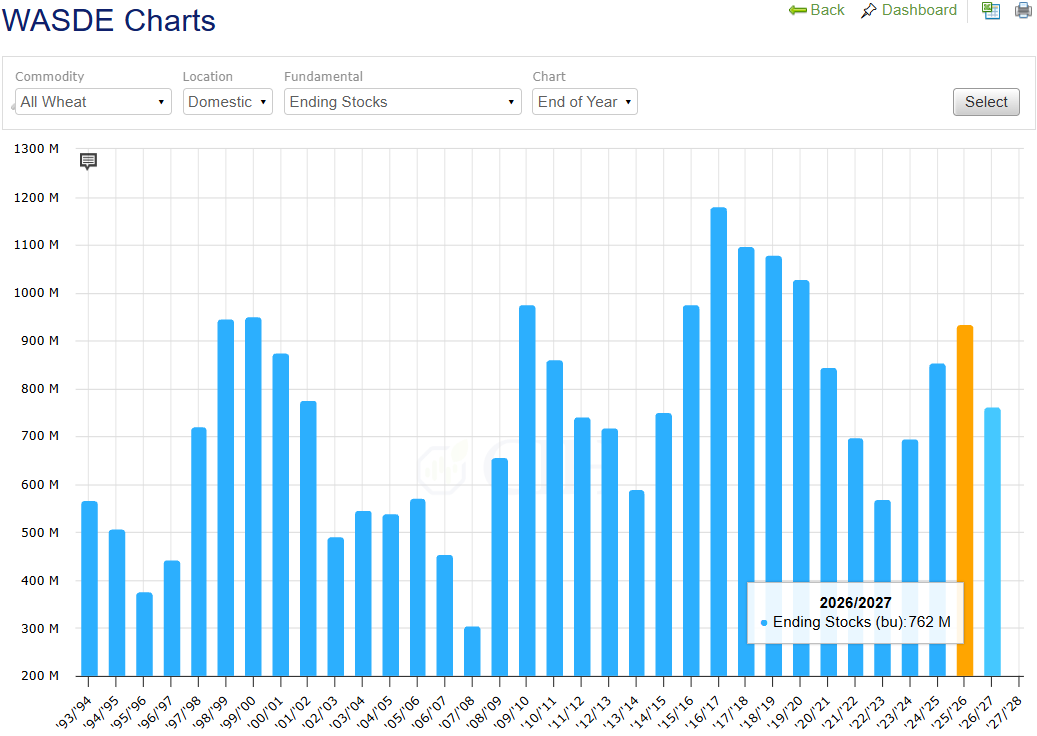

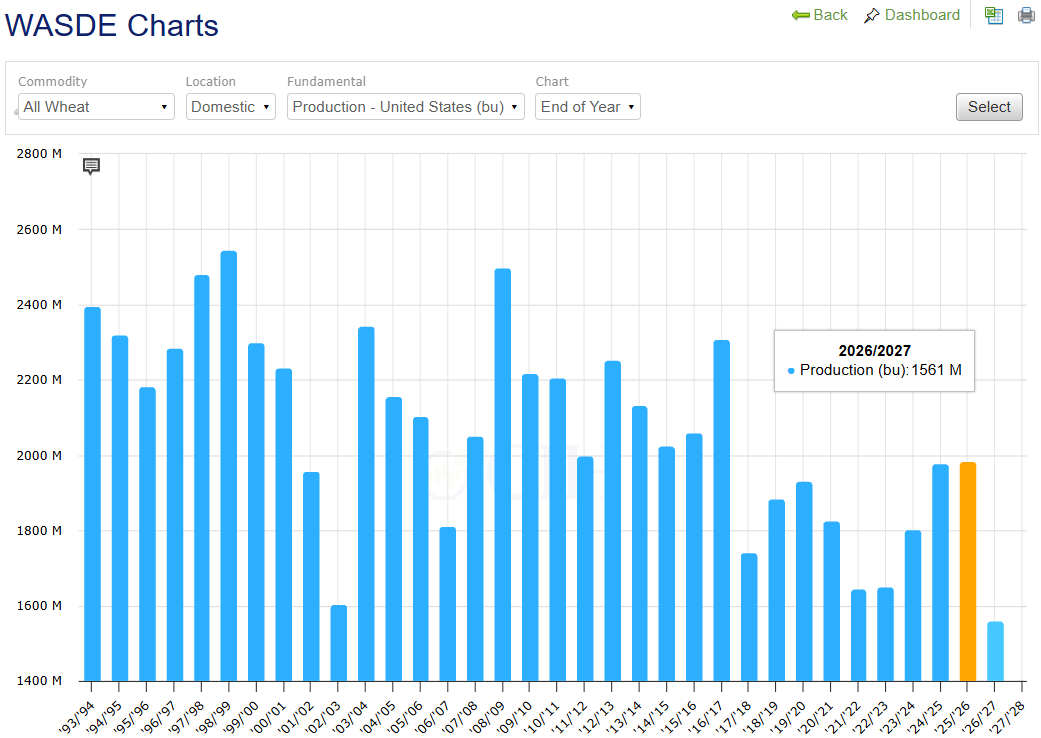

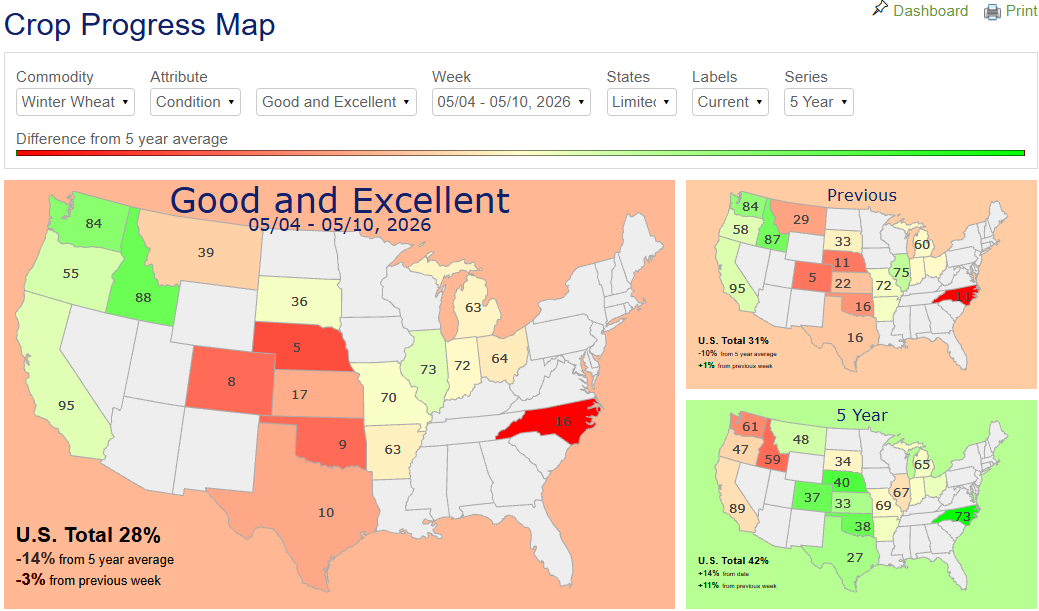

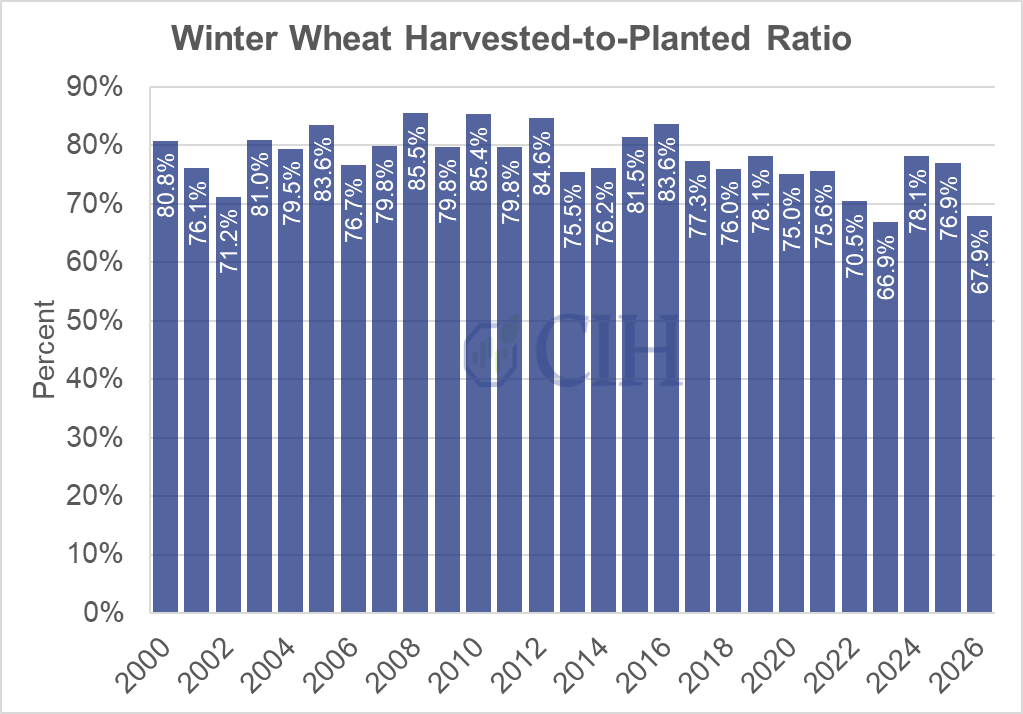

For wheat, USDA’s first 2026/27 balance sheet showed decreased production, demand, and ending stocks. All-wheat production is forecast at 1.561 billion bushels, down 424 million bushels from 2025/26 on smaller harvested area and lower yields. Yields are projected 5.8 bushels lower y/y to 47.5 bushels. For the winter wheat crop, the first survey-based production forecast came in at 1.048 billion bushels, down roughly 25% from last year on abandonment and yields. If realized, this will be the smallest wheat crop since 1972 and the smallest winter wheat crop since 1965. Winter wheat crop conditions continue to deteriorate with only 28% of the crop in good-to-excellent condition (lowest since 1996). Due to smaller production, demand is also reduced on expected higher prices. Feed and residual use is expected to drop due to higher prices. Exports are projected to decline 135 million bushels to 775 million bushels. With lower supplies more than offsetting lower demand forecasts, ending stocks are projected nearly 18% lower y/y to 762 million bushels. This puts the stocks-to-use ratio at 40.7% versus 46.1% last year.

On the world side, global ending stocks for the 2026/27 year are forecasted lower to 275.0 MMT with lower production more than offsetting decreases in demand. Global production is forecast 24.7 MMT lower to 819.1 MMT, still the second largest on record. USDA mentions, “A large share of the lower production is from all the major wheat exporting countries. The largest reductions are for the United States, the E.U., Argentina, and Australia.” Global feed and residual use is expected to decline due to lower supplies and higher expected prices. Food, seed and industrial use is forecast higher, particularly in India. Exports are forecast to decrease 12 MMT from last year. The stocks-to-use ratio for major exporters is expected to decline but remain within the range of the past 15 years.

Domestic wheat ending stocks forecast to drop sharply:

Wheat production issue project sharply lower supplies:

Winter wheat crop conditions:

Winter wheat crop abandonment:

World wheat production smaller y/y, first decrease in 8 years:

World wheat ending stocks down slightly from last year:

Major exporters stocks-to-use ratio down y/y: