April 02, 2026

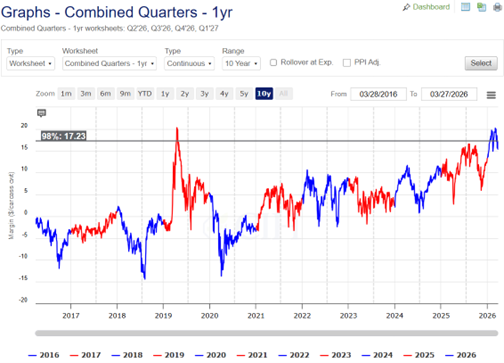

When we last wrote this column at the end of 2025, we emphasized the opportunity to protect a profitable 2026. At the time, open market margins for the following four quarters were sitting near the 97th percentile. Margins improved further in the interim, creating opportunities to scale into higher-margin coverage. Since then, geopolitical headlines have injected volatility across commodity markets. Yet despite that noise, forward-looking margins have largely returned to similar levels today.

Figure 1. Rolling 4 Quarters Margin Chart

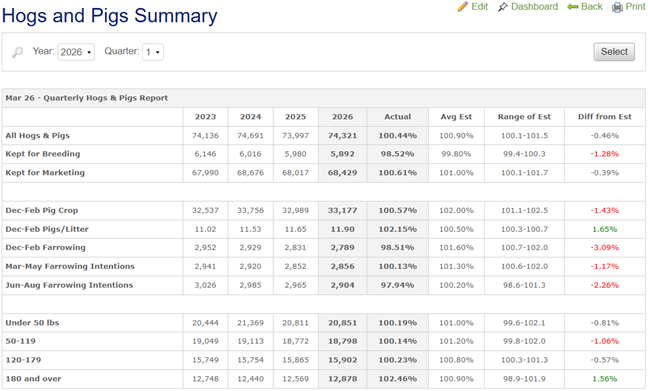

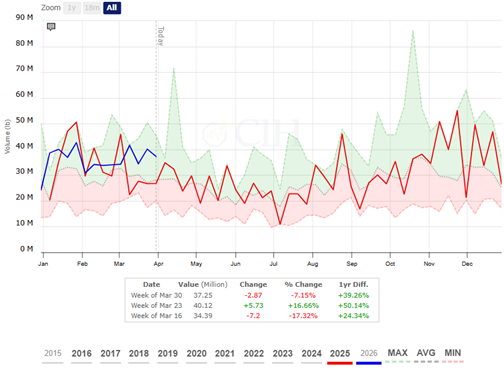

Last week’s quarterly Hogs and Pigs report leaned modestly friendly. Inventory levels were largely in line with a year ago, though the total came in slightly below pre-report expectations. Market hog inventory on March 1 was estimated at 68.4 million head, up 1 percent year-over-year and essentially in line with analyst estimates. The breeding herd told a more supportive story. At 5.892 million head, it was down 1.5 percent from March 2025, below the range of expectations, and the smallest March 1 inventory since 2014. Partially offsetting that contraction was a stronger-than-expected increase in litter rates. On the production side, recent trends have been mixed. Weekly hog slaughter has trended above year-ago levels in recent weeks, and producer-sold carcass weights continue to post modest gains. Despite these developments, year-to-date pork production remains largely in line with a year ago.

Figure 2. Hogs and Pigs Summary

Data Source: USDA NASS

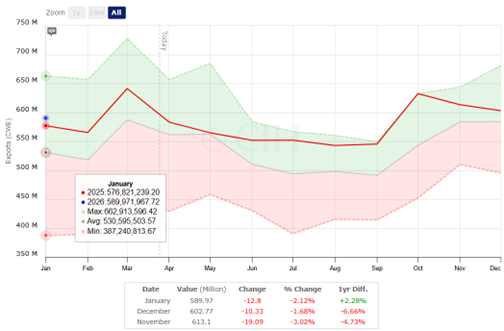

Supply tends to dominate market commentary, but it is only half the story. Demand ultimately determines how that supply is absorbed—and at what price. That makes exports central to any discussion of pork demand. The U.S. continues to demonstrate strength on the global stage, supported by product quality, producer efficiency, and sustained efforts to expand and defend market access.

Official Census Bureau data, while lagged, showed January 2026 exports up 2.3 percent year over year on a carcass-weight basis, snapping a two-month stretch of weaker comparisons late in 2025.

Figure 3. Monthly U.S. Pork Exports

Data Source: USDA ERS

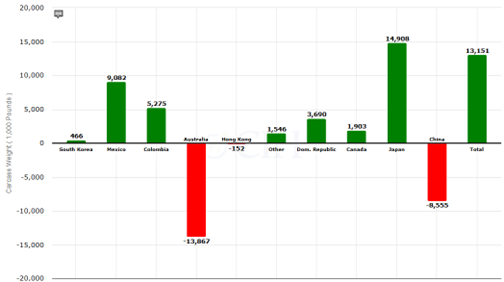

Headline totals, however, mask important shifts beneath the surface. Among key markets, Japan (+22%) and Mexico (+3.8%) led year-over-year gains. The increase in Japan is notable given the long-term erosion of U.S. market share to competitors such as Spain and Brazil, particularly in a high-value loin market. On the other side, exports declined sharply to Australia (-49.4%) and China (-20.4%). China’s total pork imports across all suppliers are expected to fall for a sixth consecutive year, reinforcing the ongoing shift away from China as a primary demand driver.

Figure 4. January 2026 Pork Exports to Major Markets

Data Source: USDA ERS

In that evolving landscape, Mexico continues to separate itself. What has emerged in the post-COVID era is a structurally stronger and more reliable export relationship. Mexico has now posted five consecutive years of record U.S. pork imports and accounts for an increasing share of total export volume. Consumption continues to expand, supported by affordability relative to beef, population growth, and ongoing supply constraints within Mexico’s domestic herd. Just as importantly, Mexico plays a critical role in carcass value. The market is a consistent buyer of hams and shoulders, helping balance the cutout and support overall pricing. The combination of strong demand, geographic proximity, and logistical advantages has made Mexico the anchor of the U.S. pork export story. That success, however, is not without risk. Recent weakness in the ham primal is causing some to question the current strength of Mexican demand in the marketplace. Concentration in a single destination creates exposure, and ongoing trade discussions, including the current anti-dumping investigation, remain an area to monitor.

Figure 5. Mexico Share of U.S. Pork Export Volume

Data Source: USDA ERS

While Mexico provides stability, developments in Europe highlight how quickly global trade flows can shift. Spain’s 2025 African Swine Fever (ASF) detection in wild boar triggered immediate trade restrictions from several key importers, including Japan, the Philippines, Malaysia, and Mexico. Other countries, such as China and South Korea, accepted regionalization protocols, limiting the broader disruption.

Current disease spread remains fluid but has not yet impacted commercial production. As the EU’s largest producer and a major global exporter, any disruption to Spain forces product to be redirected. That creates both pressure and opportunity by adding competition in some markets while opening doors in others. For the U.S., gains are most likely in premium and Asia-focused markets where access to Spanish product has been restricted. This remains a fluid situation, but it reinforces a broader theme: global pork trade is increasingly shaped by disruption, not just production.

Looking ahead, weekly export indicators point to continued strength. FAS Weekly Export Sales show solid outstanding sales to Japan and South Korea, though the dataset has become less reliable in recent years as it captures a smaller share of total exports. We continue to monitor the National Weekly Pork Report FOB Plant – Export Sales (LM_PK640), an often-overlooked but timely indicator of demand. While inherently volatile, recent trends suggest firm demand outside of North America.

Figure 6. National Weekly Pork Report FOB Plant – Export Sales

Data Source: USDA AMS

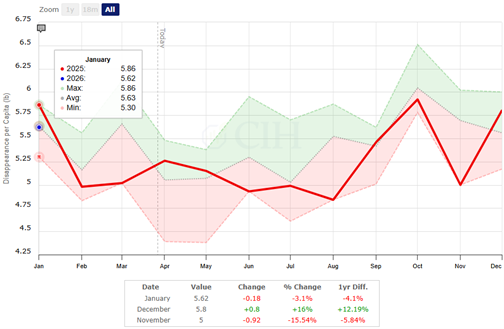

Domestically, demand appears to be improving and increasingly supportive. Per capita disappearance in December and January tracked at or above seasonal norms, a notable shift following a lackluster summer by this measure. That improvement is a welcome development for producers. Pork’s more competitive positioning relative to beef at retail is likely contributing to the firmer demand tone. This is a trend we will continue to monitor closely, particularly for its potential impact on the cutout as the market moves into the spring.

Figure 7. Monthly Pork Per Capita Disappearance

USDA projects pork exports to grow 3.1% in 2026. Achieving that will depend on a range of variables, including disease developments, trade policy, and macroeconomic conditions. From a producer standpoint, the margin environment remains historically favorable. Forward margins over the next four quarters continue to sit at attractive levels, even as volatility persists. We will gain some clarity on feed supplies with USDA’s Prospective Plantings report, but uncertainty remains. The crop is not yet planted, and weather and acreage outcomes will ultimately shape the feed side of the equation.

Given that backdrop, it may be prudent to evaluate opportunities to protect margins, both feed and hogs, while they remain elevated. Contact us to learn more about how protection can be structured to best fit your needs and to take control of your bottom line.

Trading futures and options carries a risk of loss. Past performance is not indicative of future results. Insurance coverage cannot be bound or changed via phone or email. CIH is an equal opportunity employer and provider. © 2026 CIH. All rights reserved.