March 10, 2026

Corn

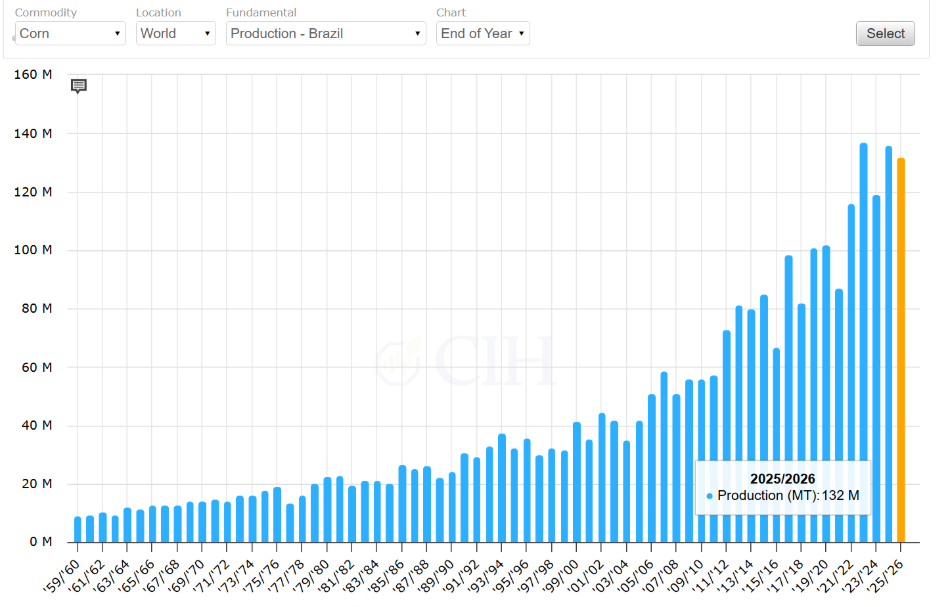

For corn, no changes were noted from the previous month. Domestic ending stocks remain at 2,127 million bu. This was below the average estimate of 2,156 but within the range of estimates of 2,027-2,428 million bu. On the world balance sheet, global production increased by 1.53 million metric tons from last month to 1,297.44 million. Of note, a 1-million-ton increase of Brazil’s crop to 132 million was offset by a 1 MMT reduction of Argentina’s crop to 52 million. Combined with an increase of 1.47 MMT to beginning stocks, world ending stocks increased 3.77 MMT from February to 292.75 million. This was above the average trade estimate of 289.6 million but within the range of estimates (range: 287.1 – 296.0). The global stocks to use ratio is now projected at 22.5% vs 22.2% in February.

Argentina’s crop was decreased 1 MMT to 52 MMT:

Brazil’s crop increased 1 MMT to 132 MMT:

Soybeans

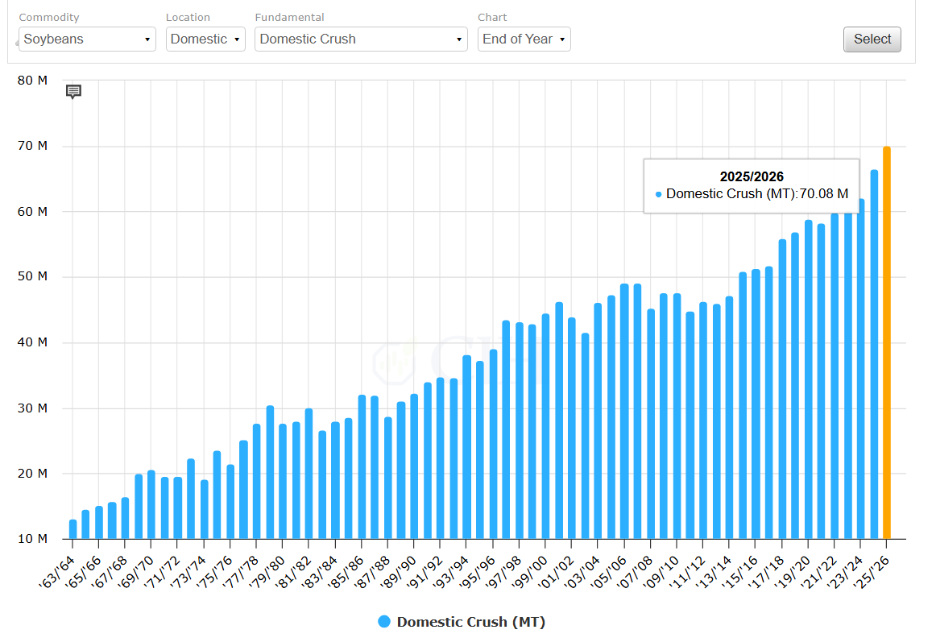

Relative to February, there’s no significant changes to the soybean domestic balance sheet. Ending stocks were left unchanged at 350 million bu. This was very close to the average trade estimate of 347 million (range: 265-384). Imports were raised 5 million to 25 million bushels, reflecting trade to date. Crush was raised 5 million bu to 2,575 million bu, due to higher soybean meal domestic use.

On the product balance sheet, soybean oil biofuel use was lowered 800 million lbs. to 14 billion lbs. while food, feed and other industrial use was raised 750 million lbs. to 15.05 billion lbs. This combined with lower production of 20 million lbs., raised soybean oil ending stocks 30 million lbs. to 1.782 billion lbs.

Soybean meal domestic production saw an increase of 325 thousand short tons to 61.077 million short tons while imports were raised 75 thousand short tons to 800 thousand. Domestic use increased 400 thousand short tons to 42.425 million. The average soybean price was left unchanged at $10.20/bu, while the average soybean oil price increased by 2 cents/lb. to 55 cents/lb. and soybean meal average price increased $5 to $300 a short ton.

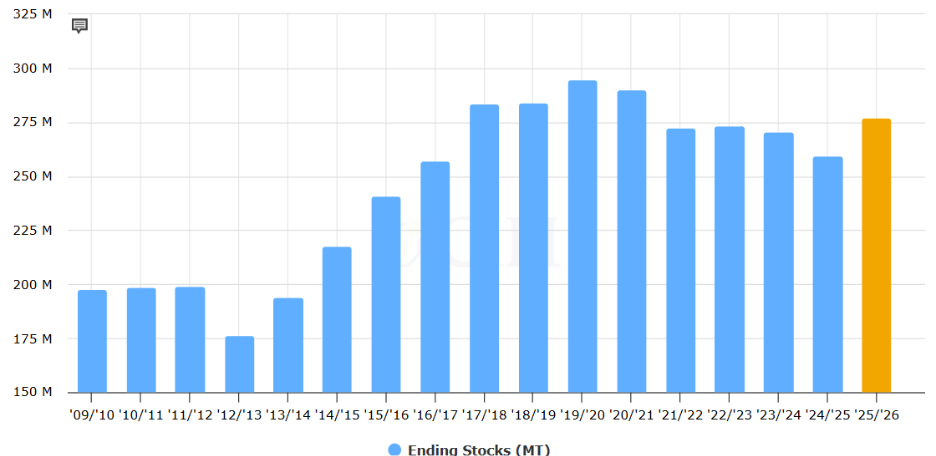

On the global balance sheet, world soybean production decreased 1 MMT from February to 427.18 million, mainly due to lower production in Argentina and Ukraine. Argentina’s production was lowered 500 thousand tons to 48 million on lower yield partly offset by higher area. Ukraine production is reduced by 500 thousand tons to 5.5 million on lower area. Global ending stocks decreased 200 thousand MT to 125.31 MMT, below the average trade estimate of 124.8 MMT (range: 123.3-126.0).

Domestic crush raised 5 million bushels to 2.575 billion bushels:

Argentina’s crop was lowered 500 thousand tons to 48 million tons:

Wheat

The domestic wheat balance sheet was left unchanged with the exception of the average farm price being raised 5 cents/bu. from February to $4.95/bu.

On the world wheat balance sheet, ending stocks were lowered 550 thousand tons from February to 277 MMT. This is lower than the average trade estimate of 277.5 (range: 276.6-278.5), but remains at a 5-year high. Australia’s crop was lowered 1 MMT to 36 MMT while Ukraine’s crop was raised 1 MMT to 24 MMT. Lower exports were noted for both the EU and Ukraine, down 1 MMT and 0.5 MMT, respectively. This was offset by Argentina’s exports being raised 1.5 MMT to a record 19.5 million, as its wheat remains the world’s lowest-priced among major exporters according to USDA.

World wheat ending stocks were lowered 550 thousand tons from February to 277 MMT:

Argentina’s wheat exports increased 47% year over year to 19.5 MMT: