September 29, 2025

Pork producer profitability continues to hold firm, buoyed by strong domestic demand and a general reluctance from producers to aggressively expand production. With cooler weather, modestly higher hog slaughter, and improving herd health, the tight supply environment that’s persisted since early summer could potentially ease. A relatively bullish Hogs and Pigs report last week, on the other hand, could spur further market strength. As we move into the heart of autumn, here are the key supply fundamentals we’re watching with clients.

Supply Fundamentals

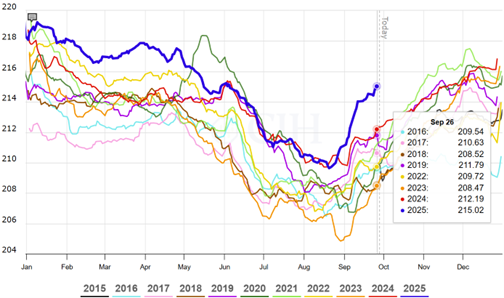

Pork production since early June was lower than implied from the June Hogs and Pigs report. Pork production under Federal inspection is down 2.1 percent year-to-date, although 2025 has had two fewer slaughter days in that calculation than last year. After tracking near year ago levels through most of the summer, producer sold hog weights are making their seasonal climb higher at a quicker pace than usual.

Figure 1. Producer Sold Hog Weights

As temperatures cool and new crop feed becomes available, the rate of increase in carcass weights will be a data point we keep an eye on through the end of the year.

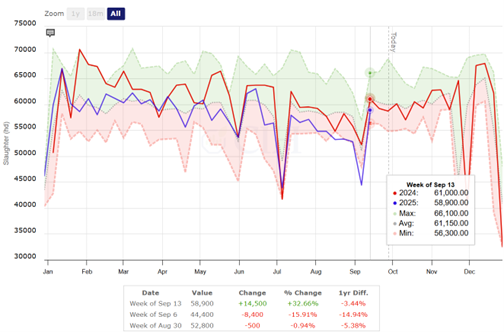

Another notable recent trend is the relative decline in sow slaughter. Weekly sow slaughter has remained below last year’s levels for much of the year. Year-to-date sow slaughter is down 5.8 percent, with the most recent weeks posting even larger reductions from year ago slaughter levels.

Figure 2. Weekly Sow Slaughter

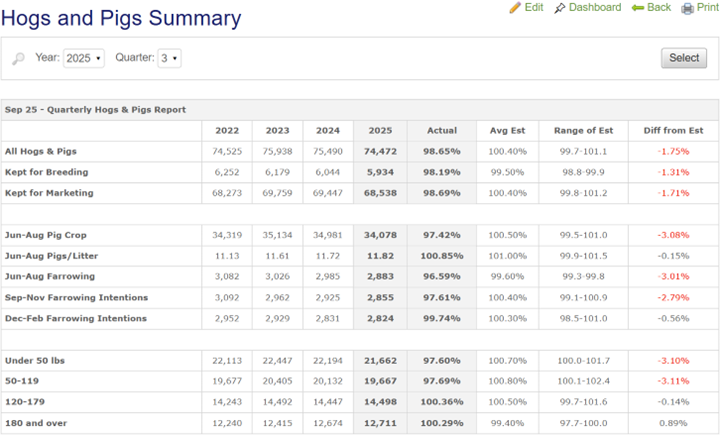

Four times a year, USDA’s Hogs and Pigs report offers a detailed snapshot of U.S. swine inventories and breeding intentions, providing critical insight for forecasting pork production and guiding market decisions. While subject to future revisions, it remains the most comprehensive assessment of current and expected animal supplies. The September 1 sow herd was estimated at 5.93 million head, down 2 percent from last year and below the low end of analysts’ pre-report expectations. Lighter-weight inventories also came in well under the average estimate, a development that could lend support to the market heading into Q1 2026.

Figure 3. Hogs and Pigs Summary

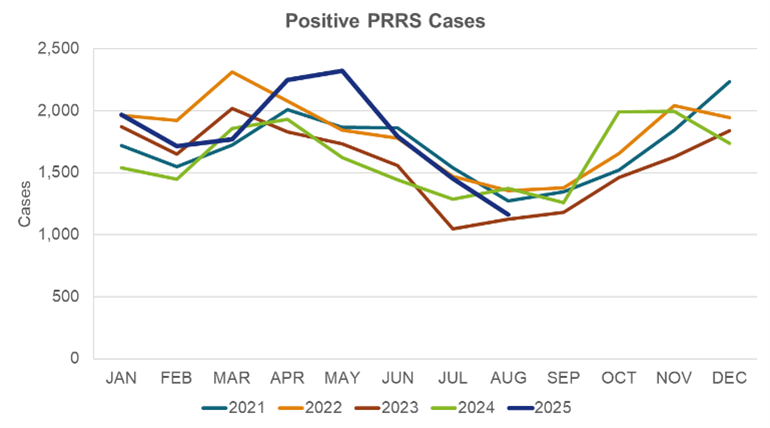

Data from the Swine Health Information Center’s Disease Reporting System suggests herd health is improving. Positive PRRS cases have seasonally fallen and, as of August, were near the lower end of the five-year range. Client feedback confirms this trend. We will continue monitoring this critical data and its impact on pig flow, and perhaps most importantly, how quickly the incidences pick up again as we head into the colder winter months.

Figure 4. Positive PRRS Cases

On the trade front, tensions remain with major U.S. pork export partners, and new risks are emerging elsewhere. On September 5, China announced temporary tariffs on a range of EU pork products, including chilled and frozen meat, offal, and pork fat. Spain, currently China’s top supplier, could face the greatest impact. While the tariffs don’t block EU pork from entering China, they could displace product onto the global market.

News reports also indicate the Chinese government has convened major pork producers in their country to discuss measures to reduce pork production by reducing their sow herd by January. While the size of the reduction is tough to discern, it could provide a boost to future export demand for U.S. product, should a trade deal or truce come to fruition.

Margin Outlook and Considerations

Every producer faces unique costs, pricing structures, and risk tolerances, but overall, the margin outlook remains exceptionally strong. Demonstration hog operation margins for the next four quarters sit in the 100th percentile of profitability over the past decade—an extremely rare opportunity to secure favorable returns and reduce risk.

Figure 5. Rolling 4 Quarters Margin Chart

That said, these margins could quickly erode if feed costs rise, hog prices fall, or both. While it may be tempting to lock in futures-based coverage, this isn’t the right strategy for everyone. Many producers remain bullish and face capital or cash flow constraints that make capital intensive tools less attractive. Fortunately, alternatives exist that provide downside protection while preserving upside opportunity.

On the feed side, producers are capitalizing on seasonal lows and favorable basis opportunities, especially in the Western Corn Belt, to secure physical purchases through late 2025 and into the first half of 2026. On the revenue side, Livestock Risk Protection (LRP) remains a popular choice. LRP offers protection against lower hog prices while allowing upside exposure, with premiums due only after animals are sold.

Given today’s environment, it may be wise to address both legs of the margin equation (feed costs and hog prices) by layering into flexible coverage strategies with cash flow friendly characteristics. This approach can help capture historically strong margins while maintaining the ability to benefit from further favorable moves.

Contact us to discuss how to take advantage of current opportunities and put your operation in control of its bottom line.