April 09, 2026

This report was considered neutral for corn and soybeans and slightly negative for wheat. The market’s focus will shift to early-season planting progress and next month’s WASDE where USDA will publish it’s first balance sheet for the 2026/27 crop year.

Corn

For corn, no changes were noted from the previous month. Domestic ending stocks remain at 2,127 million bu. This was below the average estimate of 2,143 but within the range of estimates of 2,052-2,267 million bu. On the world balance sheet, global ending stocks are forecast slightly higher at 294.81 MMT. No major changes were made.

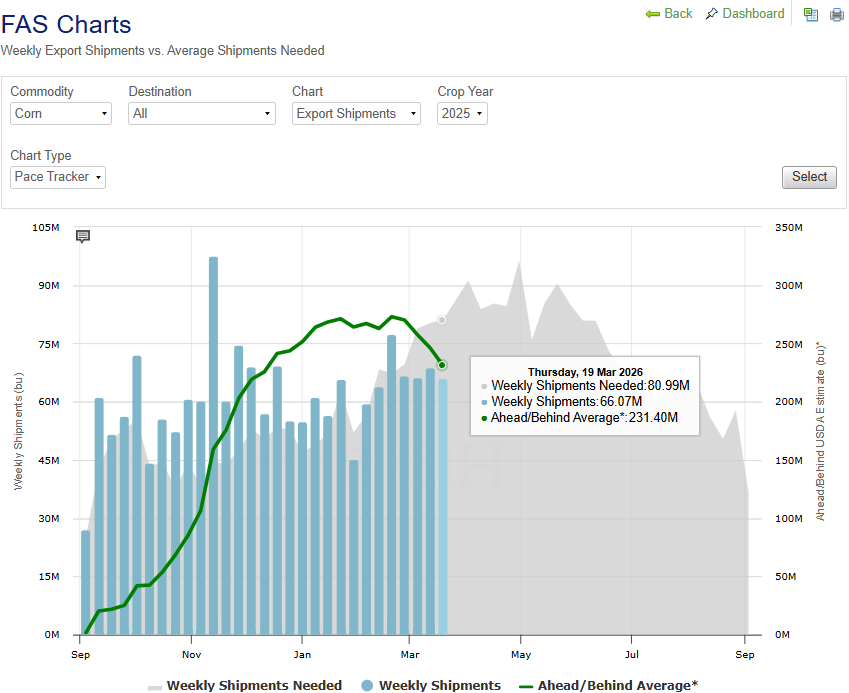

Corn exports remain on track to meet the USDA estimate:

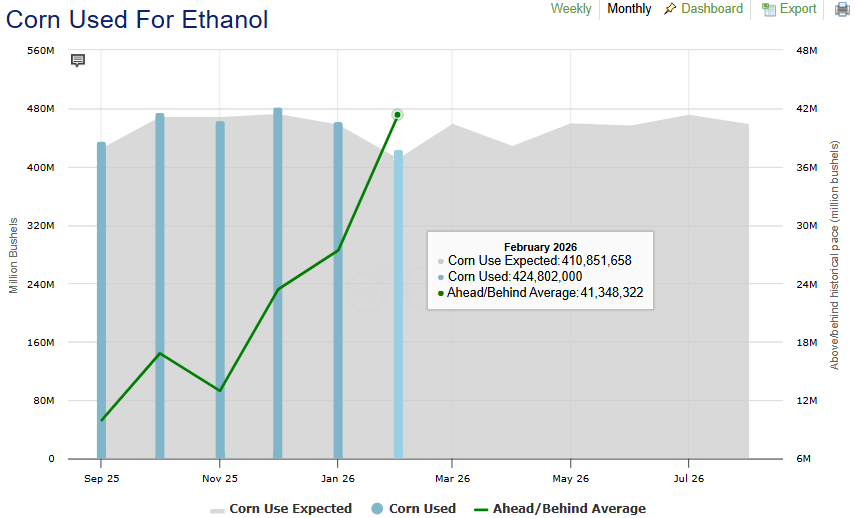

Corn use for ethanol remains on track to meet the USDA estimate:

Soybeans

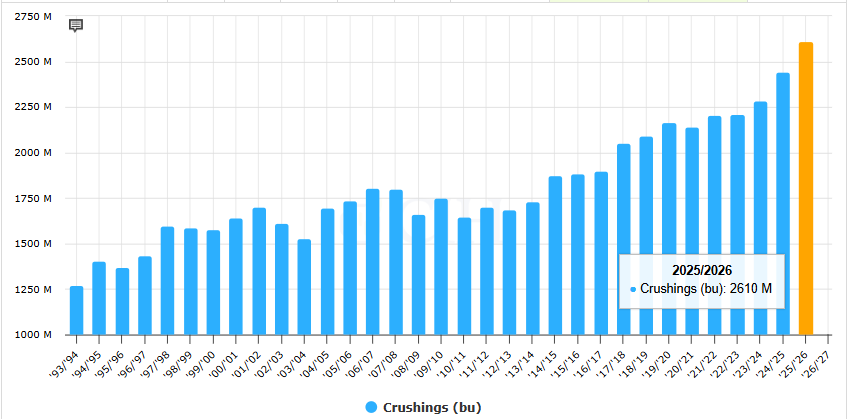

Soybean ending stocks are unchanged at 350 million bushels from March. The WAOB did make offsetting adjustments to crush and exports. Crush is raised 35 million bushels to 2.610 billion bushels, reflecting increased domestic soybean meal disappearance. Exports were lowered 35 million bushels reflecting the pace to date and increased competition from South America. On the product side of the balance sheet, soybean oil production is raised 410 million pounds due to the higher crush rate while imports are lowered by 50 million pounds. Use is forecast 300 million pounds higher for food, feed and other industrial use.

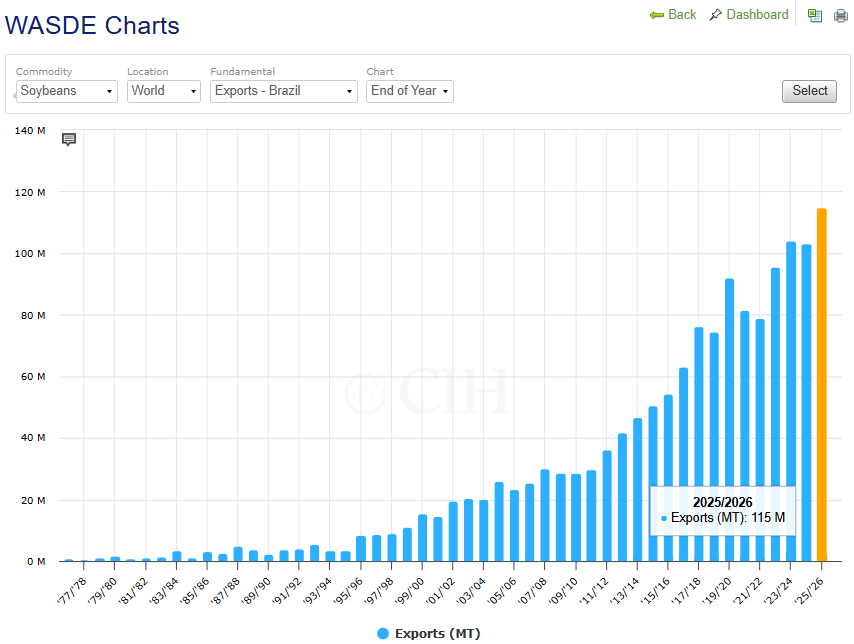

On the global balance sheet, world ending stocks are projected down slightly from last month. Brazilian exports are increased to 115 MMT.

Domestic crush raised 35 million bushels to 2.610 billion bushels:

Brazil’s exports are increased by 1.0 MMT:

Wheat

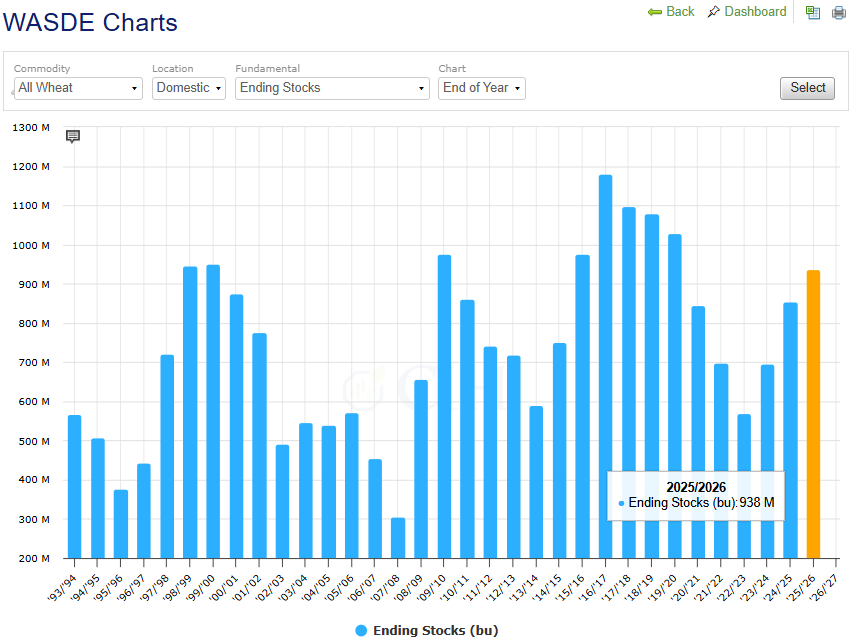

The domestic wheat balance sheet called for lowered seed use and higher imports. Seed use is decreased 1 million bushels, reflecting the lower planted area expectation as reported in the March 31 Prospective Plantings Report. Imports were raised based on current Census data through February. Ending stocks are projected 7 million bushels higher to 938 million bushels.

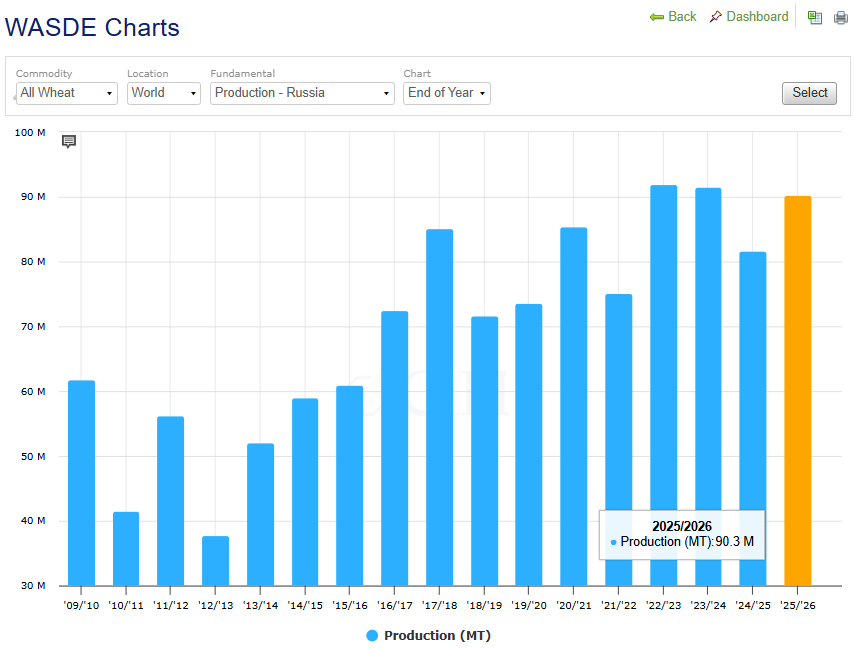

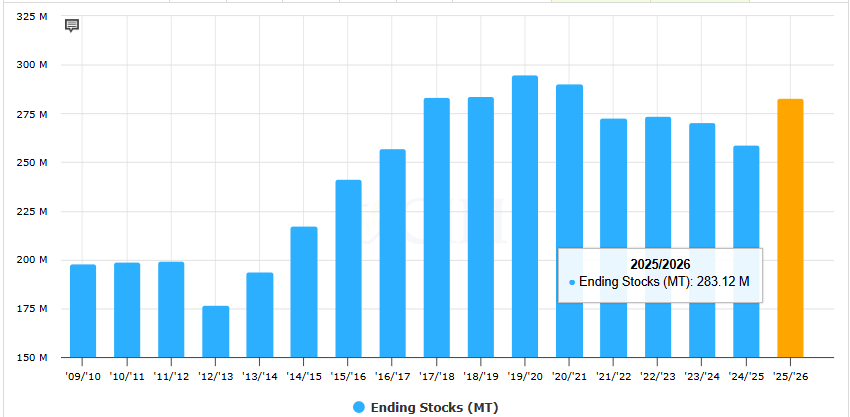

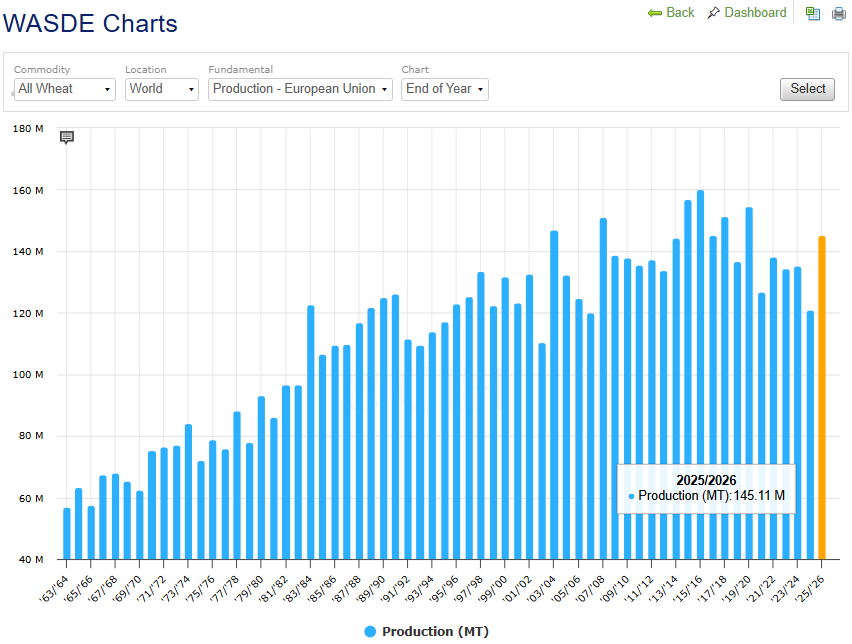

On the world wheat balance sheet, supplies are forecast higher due to increased production in the E.U. and Russia and lower usage in India. Production for E.U. and Russia are both raised roughly 1 MMT. India’s usage was lowered 4.7 MMT. USDA states the change is due to, “That country’s government wheat stocks data for the first 11 months of its marketing year indicate higher stocks than previously estimated implying less domestic use.” As a result, world ending stocks are forecast up 6.2 MMT to 283.12 MMT.

Domestic wheat ending stocks forecast to be highest since 2019/20:

World wheat ending stocks were raised 6.2 MMT to 283 MMT, up 9% y/y and highest since 2020/21:

E.U. Production highest since 2019/20:

Russian production at similar levels seen in 2022/23 and 2023/24: