February 10, 2026

Relative to pre-report trade expectations, today’s report was neutral to bullish for corn, neutral soybeans, and neutral to bearish for wheat. With last month’s report including final production figures for the corn and soybean crops, only demand figures were adjusted in the domestic balance sheet this month. As expected, crop production estimates were adjusted in South America, with lower corn output and higher soybean production featured. Market attention will continue focus on harvest progress in South America, with production estimates still subject to change in coming reports pending field results from Brazil and Argentina, along with the pace of export sales and shipments as increased competition is expected from the region as these supplies hit the global marketplace. Attention will also begin to shift towards the new-crop growing season in the U.S., with planting and field preparations already underway in southern Texas.

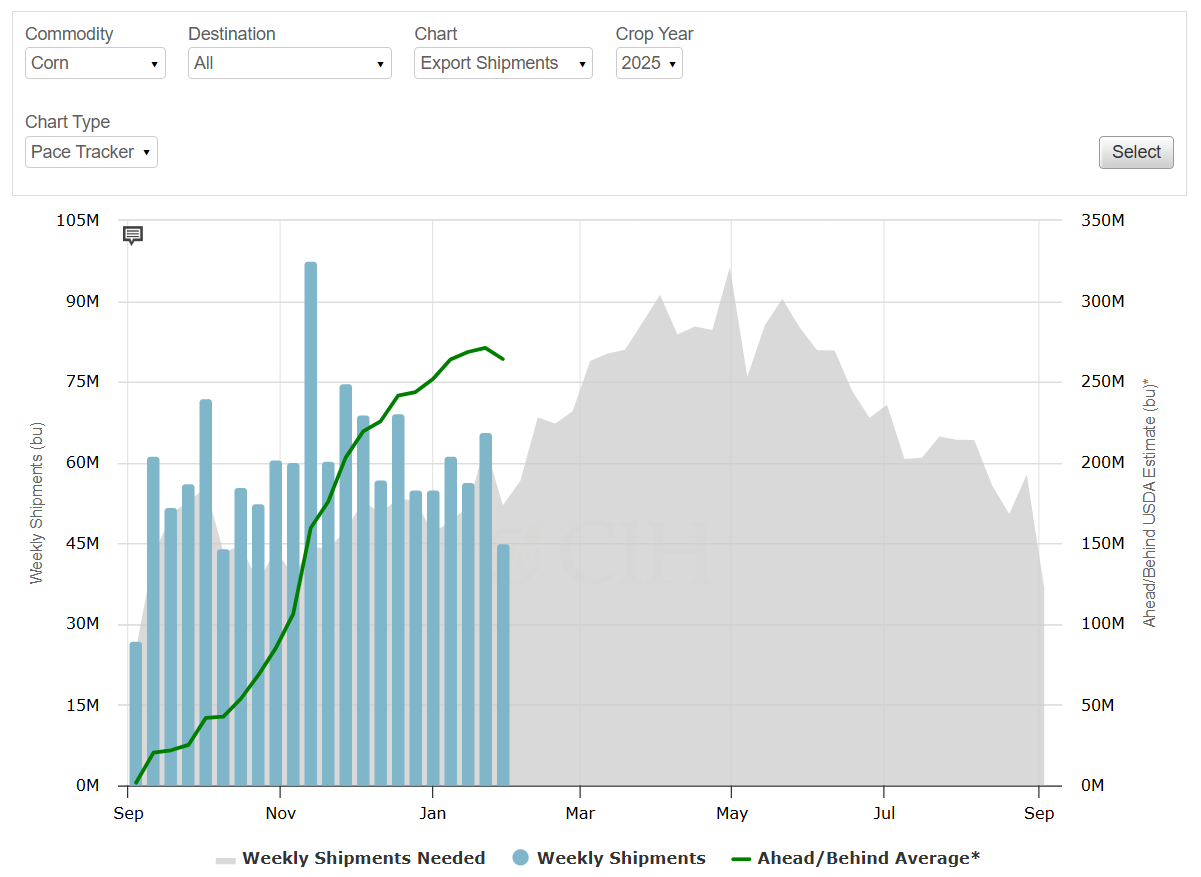

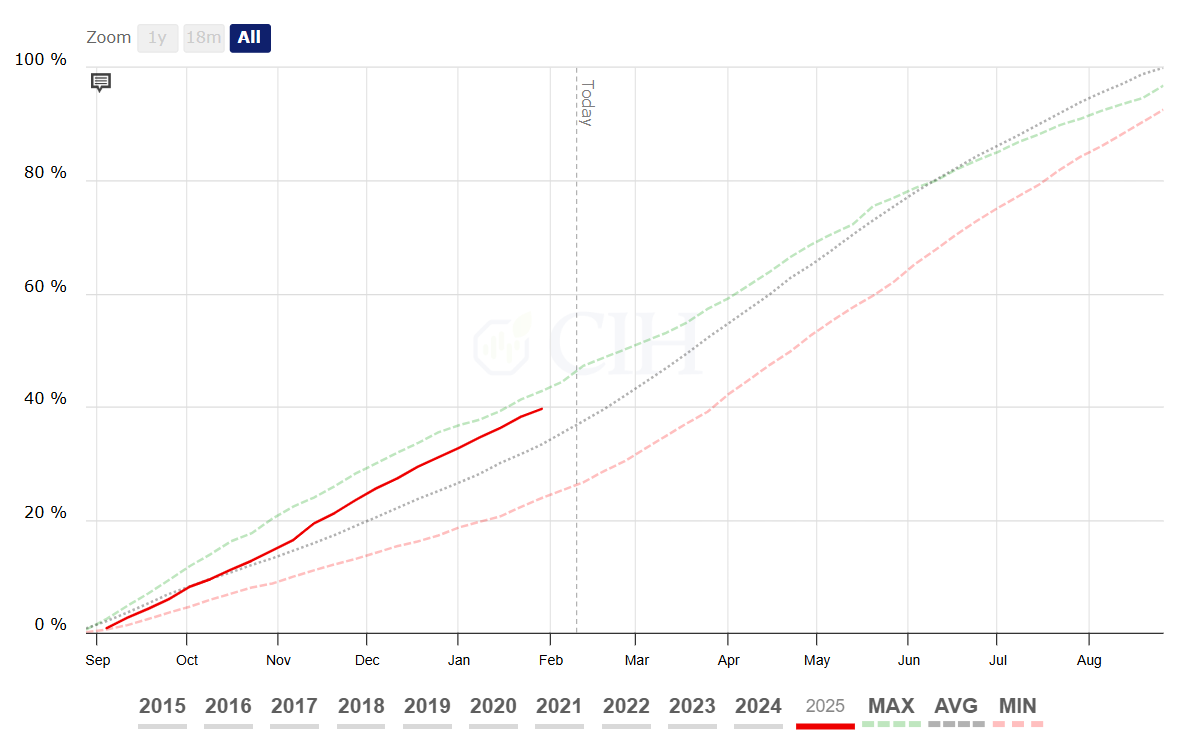

For corn, the domestic 2025/26 balance sheet called for higher exports and lower ending stocks. USDA raised the export projection by 100 million bushels to 3.3 billion bushels reflecting sales and shipments to date. Export sales and inspection data continued to show robust foreign demand during January and imply total shipments during the September-January period will most likely exceed 1.3 billion bushels according to the verbatim text of the USDA report. With no other changes noted to the domestic balance sheet, ending stocks were lowered by a similar amount to 2.127 billion bushels. This was below both the average trade guess of 2.26 billion and the pre-report range of estimates (range: 2.177-2.452). The world balance sheet featured lower ending stocks with most of that coming from the U.S. World ending stocks were projected at 289 MMT, down 1.9 million from January and below the average trade estimate of 291.3 MMT but within the range of pre-report estimates (range: 288.3-294.6).

Corn exports increased 100 million bushels to 3.3 billion bushels based on robust YTD shipments:

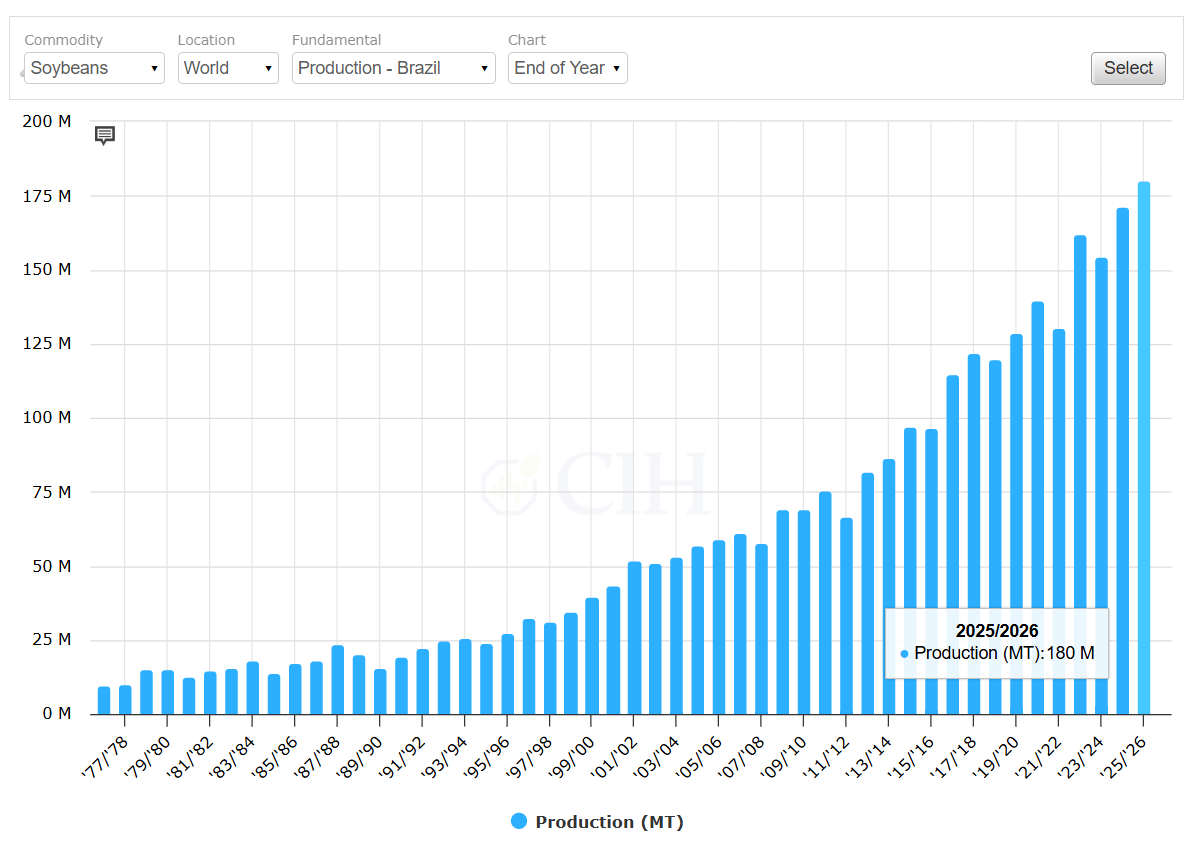

The domestic soybean balance sheet was left entirely unchanged, with ending stocks still projected at 350 million bushels which essentially matched the average pre-report trade estimate of 348 million bushels (range: 265-375). Likewise, no changes were noted to the balance sheets for the soybean products, with both meal and oil supply/demand categories matching their January estimates. The world soybean balance sheet featured higher production for Brazil and Paraguay, with the former raised 2 million tons to 180 million and the latter 500,000 tons to 11.5 million. Except for SEA imports rising 150,000 tons to 10.95 million, no other changes were noted this month. Global soybean ending stocks were raised 1.1 million tons to 125.5 million, equal to the average trade guess with a range of estimates between 123.2 – 127.0 million.

Brazil soybean production raised to a new record of 180 million metric tons:

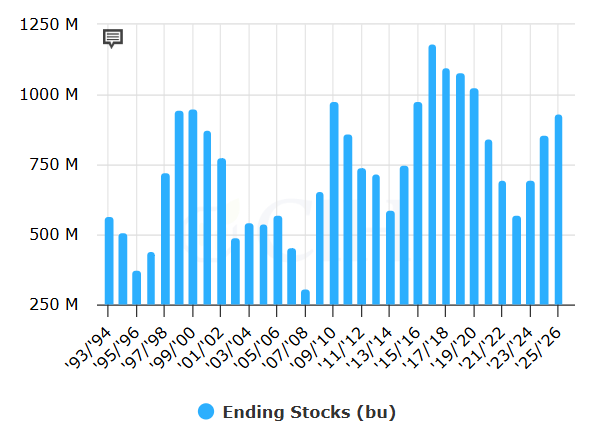

The domestic wheat balance sheet featured a slight rise in ending stocks with modestly lower domestic use. Food use was lowered 5 million bushels as indicated by the NASS Flour Milling Products report, issued on February 2. Ending stocks were raised by a corresponding amount to 931 million bushels, 9% higher than last year and the largest since 2019/20. The ending stocks projection was above the average trade forecast of 916 million bushels, as well as outside the range of pre-report estimates (range: 876 – 926). The world balance sheet featured slightly lower supplies, fractionally greater consumption, higher trade and lower ending stocks. Argentina’s production was raised again to a record 27.8 million tons, but this was more than offset by lower production for Turkey and Mongolia. Exports for Argentina and Canada were raised by 2 million and 1 million tons, respectively, but lowered 1 million tons for the EU. Imports were raised 800,000 tons for SEA, and world wheat ending stocks were lowered 800,000 tons to 277.5 million, below analysts’ average pre-report estimate of 278.3 million metric tons but within range of expectations (277.1 – 279.0 million range).

Domestic ending stocks of 931 million bushels would be the highest since 2019/20:

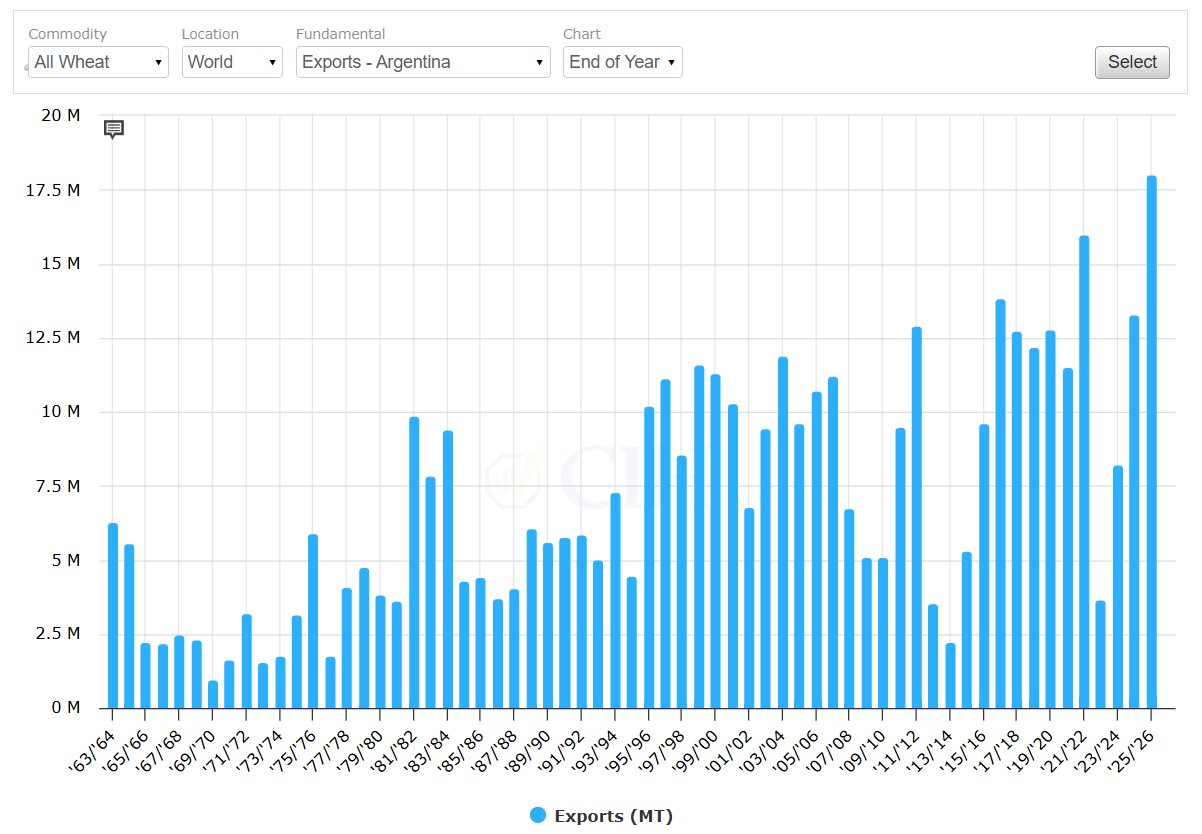

Argentina’s exports forecast at a record 18 million tons: