January 12, 2026

Today’s report was bearish for corn, soybeans, and wheat relative to pre-report expectations. The January report included final production figures for the corn and soybean crops along with winter wheat seedings and quarterly grain stocks as of December 1. Generally, all the data leaned bearish with production and inventory levels above the average of analysts’ estimates, with many of the figures also above the range of pre-report estimates. In summary, the report featured looser balance sheets for all three crops with growing stocks expected in both the domestic and global markets. Market attention will continue focus on South American crops with production growing in Brazil and Argentina along with the pace of export sales and shipments as increased competition is expected to build from growing supplies in the Southern Hemisphere over the coming weeks and months.

Corn

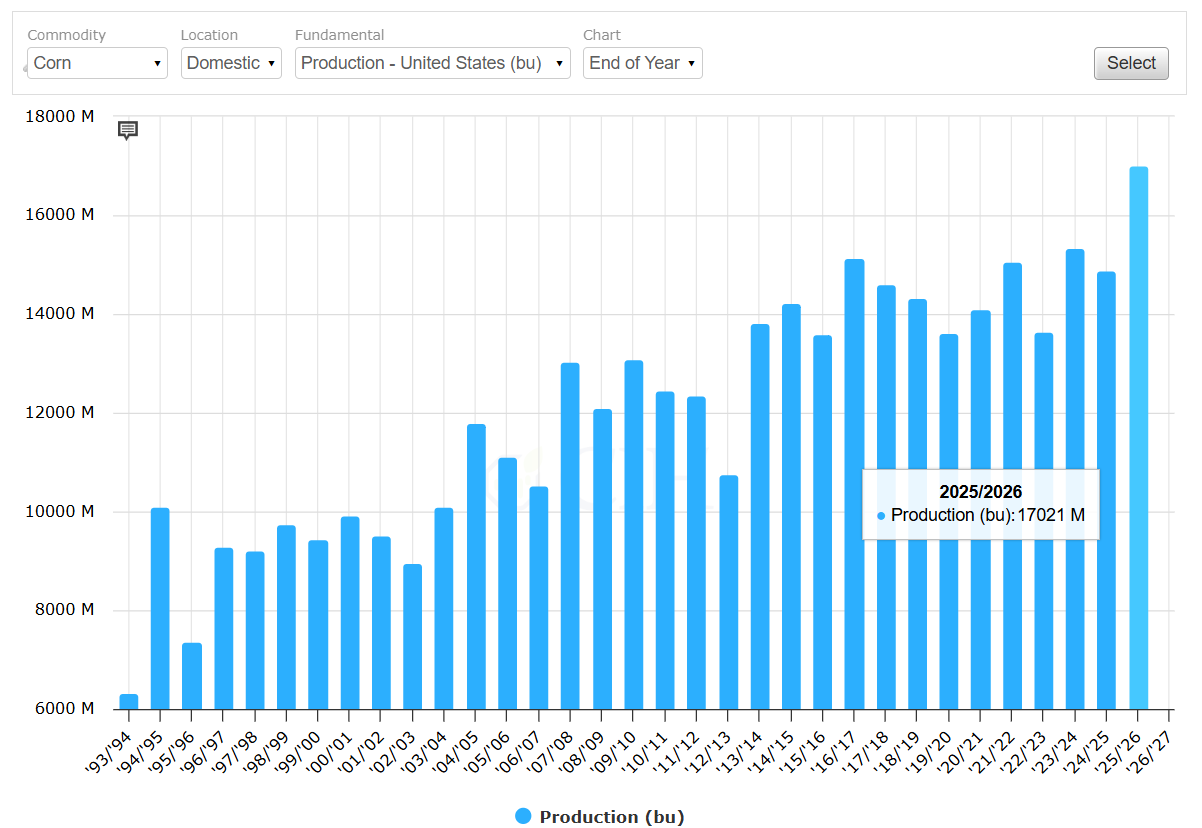

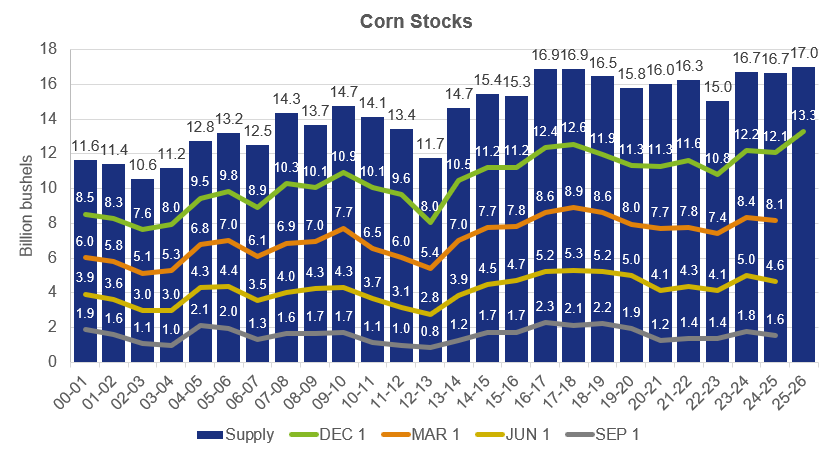

For corn, the domestic 2025/26 balance sheet called for higher production and stocks with increased demand only offsetting a portion of the larger supply. USDA raised both planted and harvested corn acres by 100,000 and 1.3 million, respectively, with yield also forecast up 0.5 bushels per acre from the previous forecast to 186.5 BPA. Total production was raised 269 million bushels from December to 17.021 billion, a new record high that well exceeds to previous record set in 2023 by 1.7 billion bushels. Total corn production, yield and harvested acres all came in above the range of pre-report estimates. Corn production at 17.021 billion bushels compares to the average trade guess of 16.544 billion (range: 16.353-16.724), yield at 186.5 bushels per acre compares to the average trade guess of 183.9 bushels (range: 182.0-185.3), and harvested acres at 91.3 million compares to the average trade estimate of 89.9 million (range: 89.3-90.4). Since the July WASDE, harvested area has surged 4.5 million acres. December 1 corn stocks were estimated at 13.282 billion bushels compared to the average trade guess of 13.040 billion (range: 12.275-13.369), with feed and residual use projected up 100 million bushels from last month to 6.2 billion based on indicated disappearance during the Sep-Nov quarter as reflected in the Grain Stocks report. Food, seed and industrial use is forecast down slightly by 10 million bushels from last month, reflecting reductions in the amount of corn used for glucose, dextrose and high fructose corn syrup. With supply increasing more than projected demand, ending stocks were forecast up 198 million bushels to 2.2 billion, with the average farm price raised $0.10 from December to $4.10/bushel.

On the World balance sheet, global corn production was forecast up 13.05 million metric tons from last month with a 6.24 million ton increase in China’s production to a record 301.2 million tons adding to the increased supply from the U.S. The Chinese production estimate reflected the latest data from the National Bureau of Statistics with global corn ending stocks projected up 11.8 million tons from last month to 290.9 million which was well above the average trade estimate of 280.0, and above the range of pre-report estimates (range: 277.0-283.0).

Corn production at 17.021 billion bushels would be a new record high, far exceeding the previous record crop in 2023:

Harvested Area at 91.3 million acres has increased 4.5 million since the July WASDE estimate:

December 1 Corn Stocks were above expectations and sharply higher than last year as well as record-high for Q1:

Soybeans

The domestic soybean balance sheet featured larger production, lower demand and higher ending stocks relative to last month. Soybean production was estimated up 9 million bushels from December to 4.262 billion (avg. 4.232; range: 4.176 – 4.296), with both planted and harvested area increased 100,000 acres each to 81.2 million and 80.4 million, respectively. Yield was left unchanged at 53.0 bushels per acre (avg. 52.7; range: 51.96 – 53.5), and beginning stocks were also forecast up 9 million bushels from last month. December 1 soybean stocks were estimated at 350 million bushels, higher than the average pre-report guess of 301 million but within the range of estimates (245 – 375 range). The domestic crush forecast was raised 15 million bushels from last month to 2,570 million on higher soybean meal domestic disappearance and exports, although soybean oil use for biofuel was lowered 700 million pounds to 14.8 billion on lower than expected use to date and strong use of tallow as a feedstock in recent months. Soybean exports were lowered 60 million bushels to 1,575 million on higher production and exports for Brazil. Soybean ending stocks were projected up 60 million bushels from last month to 350 million, above the average trade estimate of 301 million but within the range of estimates (245 – 375 range). The average soybean farm price was lowered $0.30/bushel to $10.20/bushel, reflecting NASS prices during Q1 of the marketing year and expectations for futures marketings and prices. The average soybean meal price was forecast down $5/ton at $295 per short ton while the average soybean oil price forecast was left unchanged at 53 cents per pound.

Global soybean production was raised 3.1 million tons to 425.7 million on higher production estimates for Brazil and the U.S., with lower production forecast in China. Brazil’s soybean production was raised 3 million tons to 178 million on beneficial weather conditions in the Central West during the peak of the growing season. Further, positive early-season conditions and consistent rainfall in the south of Brazil also bolsters yield prospects according to USDA, especially compared to previous years when the region faced drought. Global soybean exports were lowered 100,000 tons to 187.6 million as higher exports for Brazil offset lower U.S. shipments. Global soybean ending stocks were raised 2 million tons to 124.4 million, above the average trade guess of 123.1 million and outside the range of estimates (121.8 – 124.0 range) based on higher stocks for Brazil and the U.S.

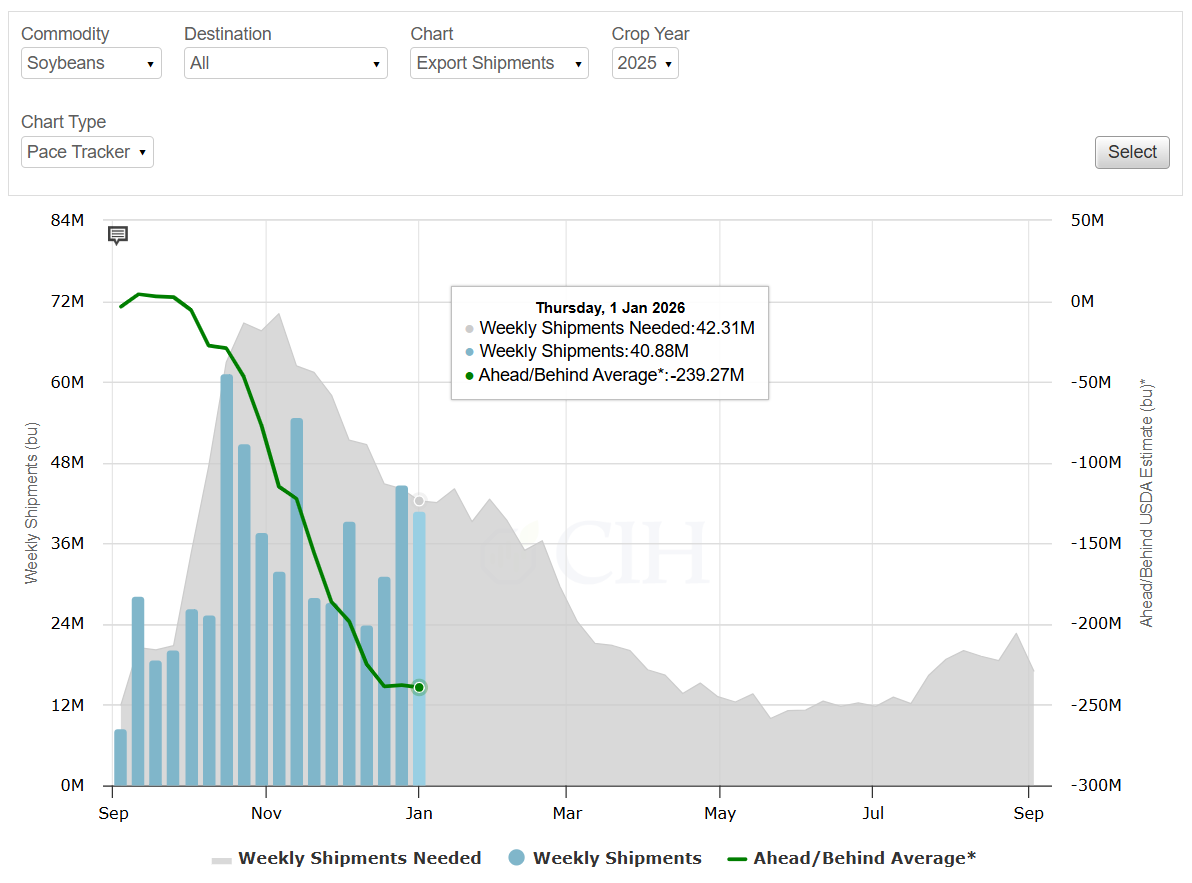

Despite a recent pickup in export commitments to China, soybean export sales remain well below the pace needed to reach the USDA forecast:

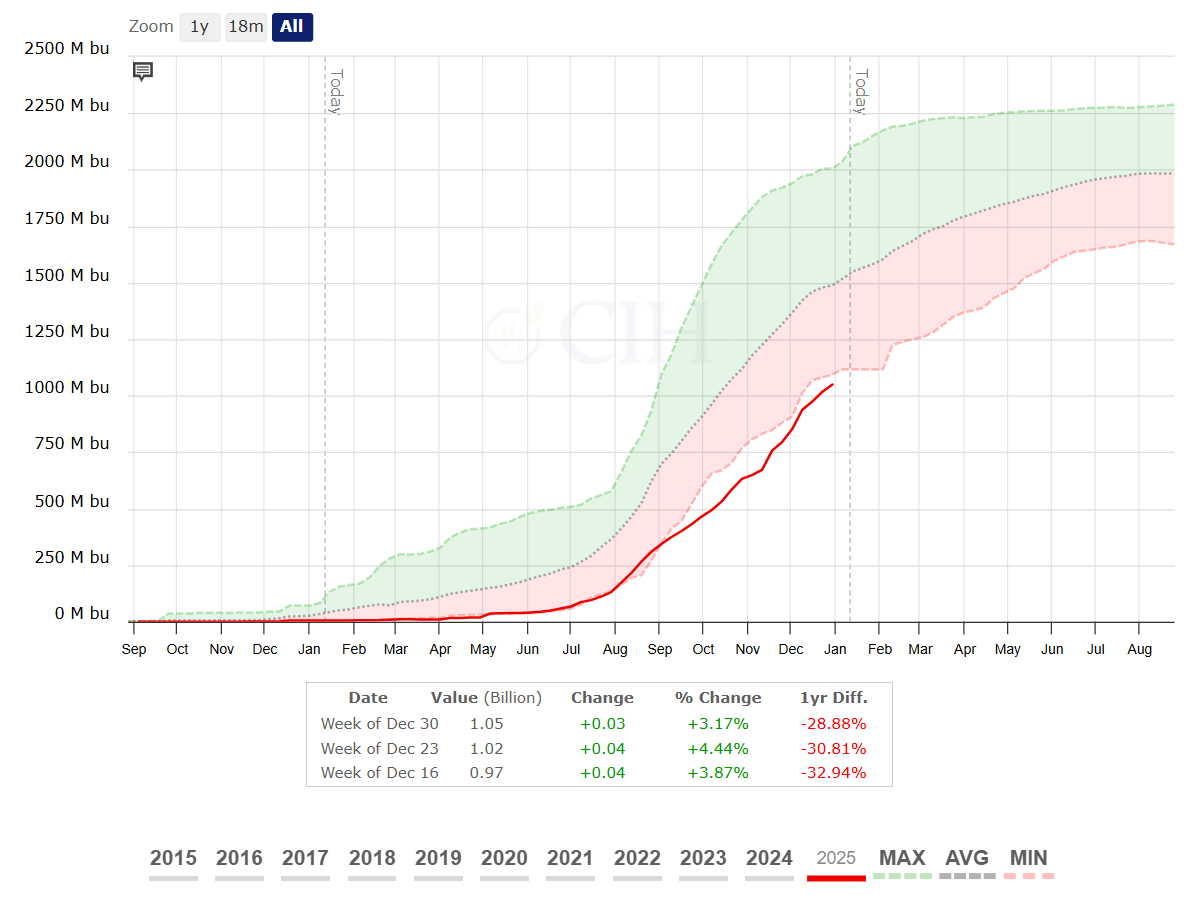

Total commitments of soybeans remain below 10-year lows despite recent sales activity to China:

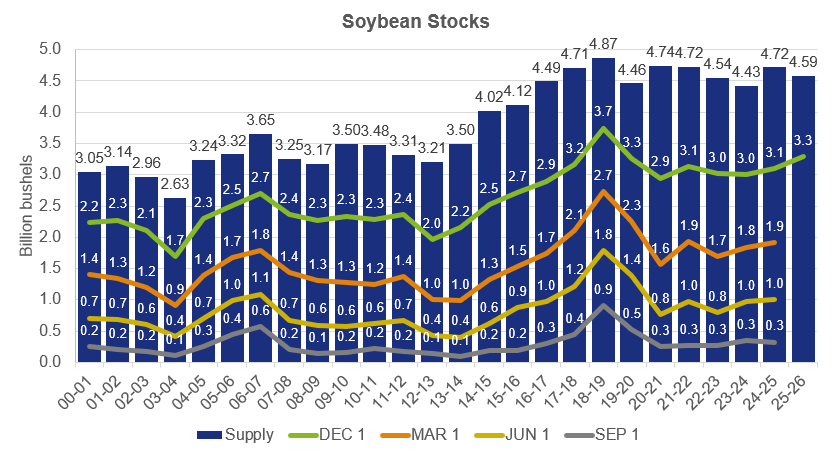

December 1 Soybean Stocks of 3.29 billion bushels are up from last year and the highest for Q1 since 2019/20:

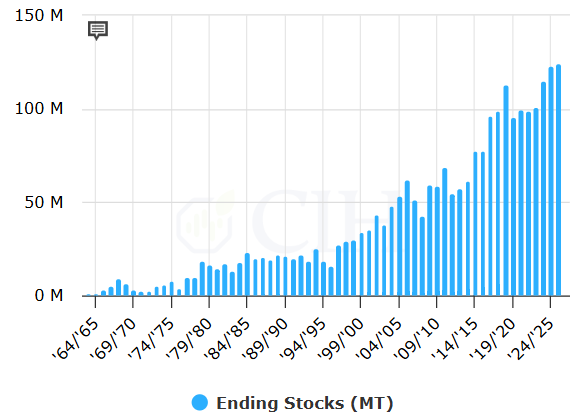

World Soybean Ending Stocks at 124.4 million tons would be a new record high:

Wheat

While winter wheat seedings were higher than the average trade estimate, they were within the range of forecasts and generally neutral. All Winter Wheat planted area was estimated at 33.0 million acres (avg. 32.3; range: 31.0 – 33.4), with hard red winter wheat estimated at 23.5 million acres (avg. 23.0; range: 22.0 – 24.0), soft red winter at 6.14 million (avg. 5.9; range: 5.5 – 6.1), and white winter wheat at 3.36 million (avg. 3.5; range: 3.2 – 3.7). December 1 wheat stocks were estimated at 1,675 million bushels, above the average trade guess of 1,636 million but within the range of estimates (1,590 – 1,696 range). On the domestic balance sheet, beginning stocks were raised 4 million bushels on revisions from the Grain Stocks report, while feed and residual use was lowered 20 million bushels to 100 million based on smaller than expected Q1 disappearance and residual indicated in the same report. Seed use was lowered 1 million bushels to 61 million, based partly on the NASS Winter Wheat and Canola Seedings report. Exports were left unchanged at 900 million bushels, and ending stocks were raised 25 million bushels to 926 million which was above the average trade guess of 897 million bushels and outside the range of estimates (876 – 925 range). The average farm price was lowered $0.10/bushel to $4.90/bushel.

On the world balance sheet, global wheat supplies were raised 4.3 million tons to 1.102 billion based primarily on higher production for Argentina and Russia more than offsetting a reduction for Turkey. Argentina’s wheat crop was raised 3.5 million tons to a record 27.5 million, up nearly 50% from last year with more than 90% of the harvest complete. Russia’s wheat crop was raised 2 million tons to 89.5 million based on higher preliminary yields reported by Rosstat. World wheat ending stocks were raised 3.4 million metric tons to 278.3 million, above analysts’ average pre-report estimate of 276.2 million metric tons and outside the range of expectations (275.2 – 277.7 million range).

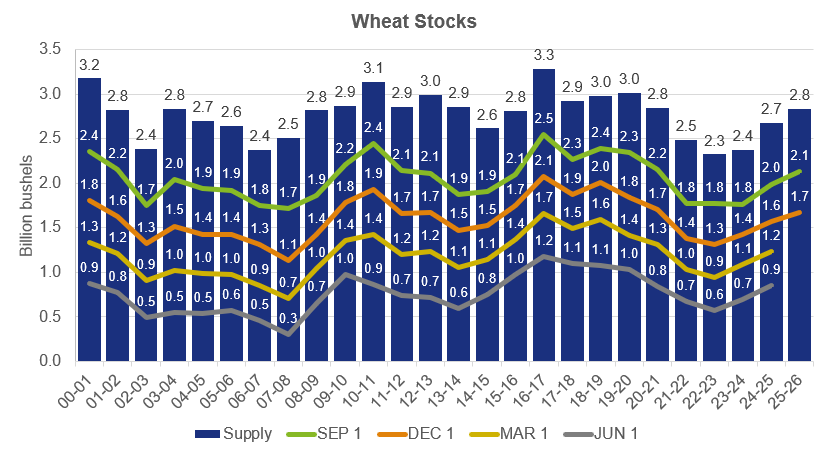

December 1 Wheat Stocks at 1,675 million bushels would be the highest for Q2 since 2020/21:

With record production in Argentina, exports are projected up sharply from last year to match the record-high in 2020/21 at 16 million tons:

Global ending stocks projected to be the largest since the 2020/21crop year: